Author: Capital Flows

Translation: TechFlow

Macro Report: The Storm Is Coming

“What important truth do very few people agree with you on?”

This is a question I ask myself every day when researching the markets.

I have models for growth, inflation, liquidity, market positioning, and prices, but the ultimate core of macro analysis is the quality of ideas. Quant funds and emerging AI tools are eliminating every statistical inefficiency in the market, compressing the advantages that once existed. What remains is macro volatility that manifests over longer time cycles.

The Truth

Let me share with you a truth that very few people agree with:

I believe that in the next 12 months, we will see a significant increase in macro volatility, on a scale that will surpass 2022, the COVID-19 pandemic, and may even exceed the 2008 financial crisis.

But this time, the source of the volatility will be a planned devaluation of the US dollar against major currencies. Most people believe that a decline in the dollar or “dollar devaluation” will drive risk assets higher, but the reality is quite the opposite. I think this is the biggest risk in today’s market.

In the past, most investors believed that mortgages were too safe to trigger systemic panic, and also ignored credit default swaps (CDS) as too complex and irrelevant. Now, the market remains complacent about the potential sources of dollar devaluation. Almost no one delves into the mechanisms of this devaluation, which could turn from a weather vane into a real risk for asset prices. You can spot this blind spot by discussing the issue with others. They insist that a weaker dollar always benefits risk assets and assume the Federal Reserve will intervene in any serious problem. It is precisely this mindset that makes a deliberately engineered dollar devaluation more likely to cause risk assets to fall, not rise.

The Road Ahead

In this article, I will detail how this mechanism works, how to identify signals when this risk emerges, and which assets will be most affected (both positively and negatively).

It all comes down to the convergence of three major factors, accelerating as we approach 2026:

-

Liquidity imbalances caused by global cross-border capital flows leading to systemic fragility;

-

The Trump administration’s stance on currency, geopolitics, and trade;

-

The appointment of a new Federal Reserve Chair, whose monetary policy will be coordinated with Trump’s negotiation strategy.

The Roots of Imbalance

For years, unbalanced cross-border capital flows have created a structural liquidity imbalance. The key issue is not the scale of global debt, but how these capital flows have shaped balance sheets to become inherently fragile. This dynamic is similar to the situation with adjustable-rate mortgages before the Global Financial Crisis (GFC). Once this imbalance begins to reverse, the structure of the system itself accelerates the correction, liquidity dries up rapidly, and the whole process becomes uncontrollable. This is a mechanical fragility embedded in the system.

It all starts with the US acting as the world’s only “buyer.” Due to the dollar’s strong status as a reserve currency, the US can import goods at prices far below domestic production costs. Whenever the US buys goods from the rest of the world, it pays in dollars. In most cases, these dollars are reinvested by foreign holders into US assets to maintain trade relations, and because the US market is almost the only option. After all, where else but the US can you bet on the AI revolution, robotics, or people like Elon Musk?

This cycle repeats endlessly: the US buys goods → pays dollars to foreigners → foreigners use those dollars to buy US assets → the US can continue buying more cheap goods because foreigners keep holding dollars and US assets.

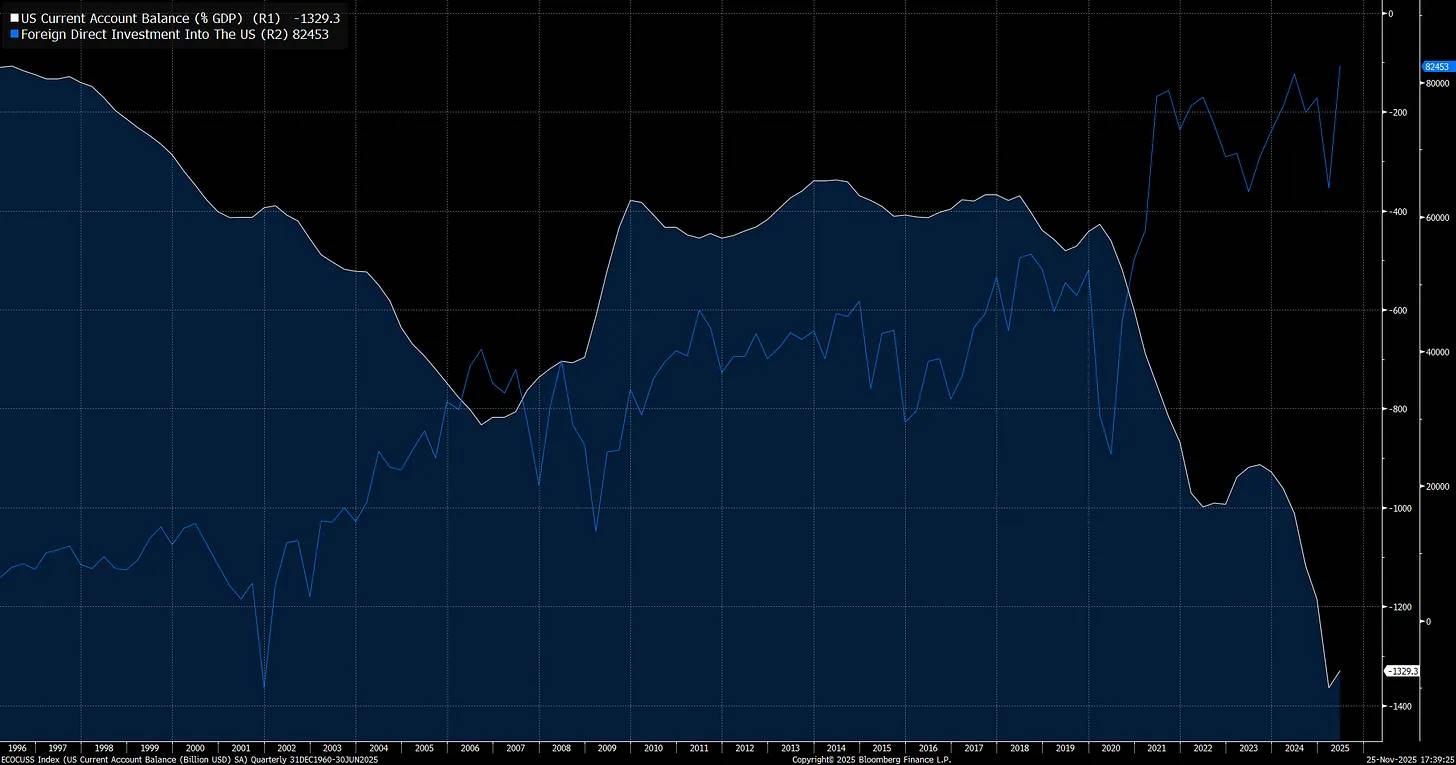

This cycle has led to severe imbalances, with the US current account (the difference between imports and exports, white line) at an extreme. On the other side, foreign investment in US assets (blue line) has also reached historic highs:

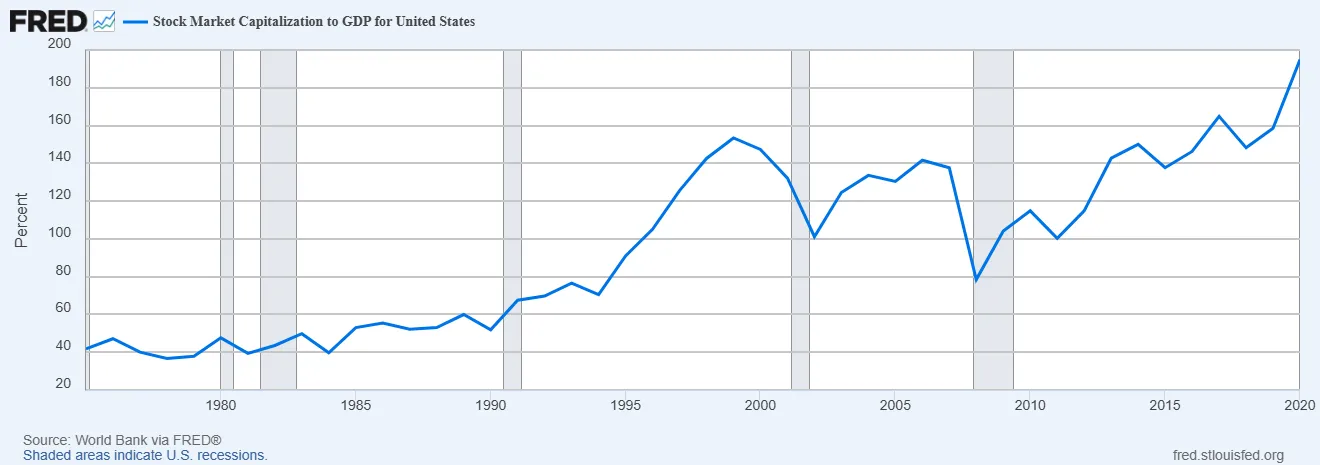

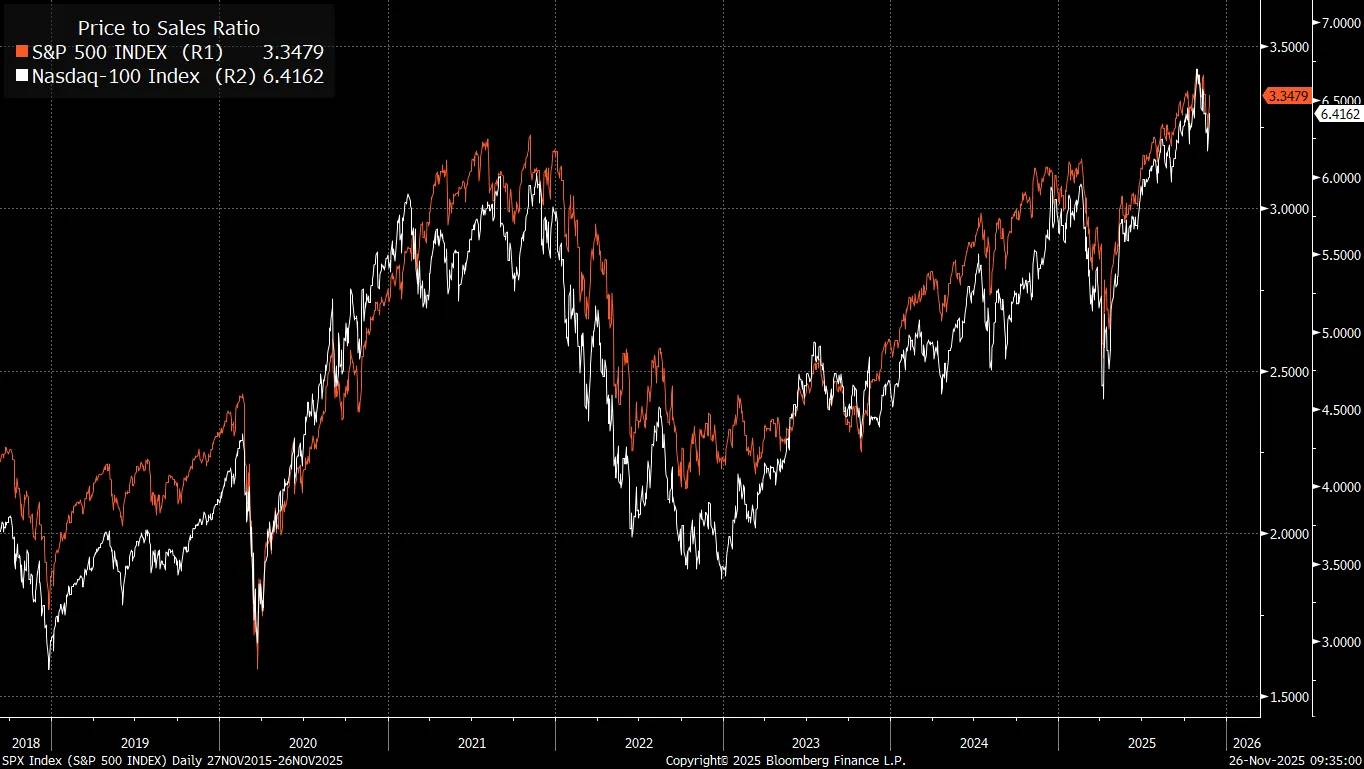

When foreign investors indiscriminately buy US assets to continue exporting goods and services to the US, this is why we see S&P 500 valuations (price-to-sales ratio) at all-time highs:

The traditional stock valuation framework comes from the value investing philosophy advocated by Warren Buffett. This approach worked well in periods of limited global trade and less liquidity within the system. However, what is often overlooked is that global trade itself expands liquidity. From an economic accounts perspective, one end of the current account corresponds to the other end of the capital account.

In practice, when two countries trade, their balance sheets guarantee each other, and these cross-border capital flows exert a powerful influence on asset prices.

For the US, as the world’s largest importer of goods, massive capital inflows are why the US market capitalization-to-GDP ratio is significantly higher than in the 1980s—the era when Benjamin Graham and David Dodd established the value investing framework in “Security Analysis.” This is not to say that valuations are unimportant, but from a total market capitalization perspective, this change is driven more by macro liquidity shifts than by so-called “irrational behavior of Mr. Market.”

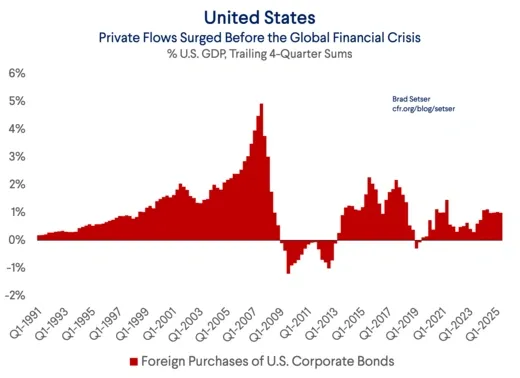

Before the Global Financial Crisis (GFC), one of the main sources driving the fragile capital structure of the mortgage market was foreign investors buying US private sector debt:

Michael Burry’s “Big Short” bet during the GFC was based on insight into fragile capital structures, and liquidity was the key factor repriced as domestic and cross-border capital flows changed. This is why I believe there is a very interesting connection between Michael Burry’s current analysis and my ongoing analysis of cross-border liquidity.

Foreign investors are injecting more and more capital into the US, and whether it’s foreign inflows or passive investment inflows, they are increasingly concentrated in the top seven stocks of the S&P 500.

It’s important to note the type of this imbalance. Brad Setser has done an excellent analysis explaining how carry trade dynamics in cross-border capital flows structurally trigger extreme market complacency:

Why does all this matter? Because many financial models today (incorrectly, in my view) assume that in the event of future financial instability—such as a sell-off in US stocks or credit markets—the dollar will rise. This assumption makes it easier for investors to continue holding unhedged dollar assets.

This logic can be simply summarized as: Yes, my fund currently has a very high weighting in US products because the US’s “dominance” in global stock indices is indisputable, but this risk is partially offset by the natural hedge provided by the dollar. Because the dollar usually rises when bad news hits. In major stock market corrections (such as 2008 or 2020, though for different reasons), the dollar may strengthen, and hedging dollar risk actually cancels out this natural hedge.

Even more conveniently, based on past correlations, the expectation that the dollar is a hedge for the stock (or credit) market also increases current returns. This provides a reason not to hedge US market exposure when hedging costs are high.

However, the problem is that past correlations may not persist.

If the dollar’s rise in 2008 was not because of its status as a reserve currency, but because the funding currency usually rises when carry trades are unwound (while the destination currency usually falls), then investors should not assume the dollar will continue to rise in future periods of instability.

One thing is indisputable: the US is currently the recipient of most carry trades.

Foreign capital did not flow out of the US during the Global Financial Crisis

This is what makes today’s world so different: foreign investors’ returns on the S&P 500 depend not only on the index’s return but also on currency returns. If the S&P 500 rises 10% in a year, but the dollar depreciates by the same amount against the investor’s local currency, it does not mean a positive return for foreign investors.

Below is a chart comparing the S&P 500 (blue line) with the hedged S&P 500. You can see that accounting for currency changes significantly alters investment returns over the years. Now, imagine what would happen if these changes were compressed into a short period. This huge risk driven by cross-border capital flows could be amplified.

This brings us to an accelerating catalyst—it is putting global carry trades at risk: the Trump administration’s stance on currency, geopolitics, and trade.

Trump, FX, and Economic Warfare

At the beginning of this year, two very specific macro changes emerged, accelerating the accumulation of potential risks in the global balance of payments system.

We have seen the dollar depreciate and US stocks fall simultaneously, a phenomenon driven by tariff policies and cross-border capital flows, not by domestic default issues. This is precisely the type of risk I mentioned above. The real problem is that if the dollar depreciates while US stocks are falling, any intervention by the Federal Reserve will further depress the dollar, which will almost certainly amplify the downward pressure on US stocks (contrary to the traditional “Fed Put” view).

When the source of the sell-off is external and currency-based, the Fed’s position becomes even more difficult. This phenomenon indicates that we have entered the “macro end game,” where currency becomes the key asymmetric pivot for everything.

Trump and Bessent are openly pushing for a weaker dollar and using tariffs as leverage to gain the upper hand in economic conflict with China. If you haven’t followed my previous research on China and its economic warfare against the US, you can watch my YouTube video titled “The Geopolitical End Game.”

The core point is: China is deliberately weakening other countries’ industrial bases, creating dependence on China, and building leverage to achieve broader strategic goals.

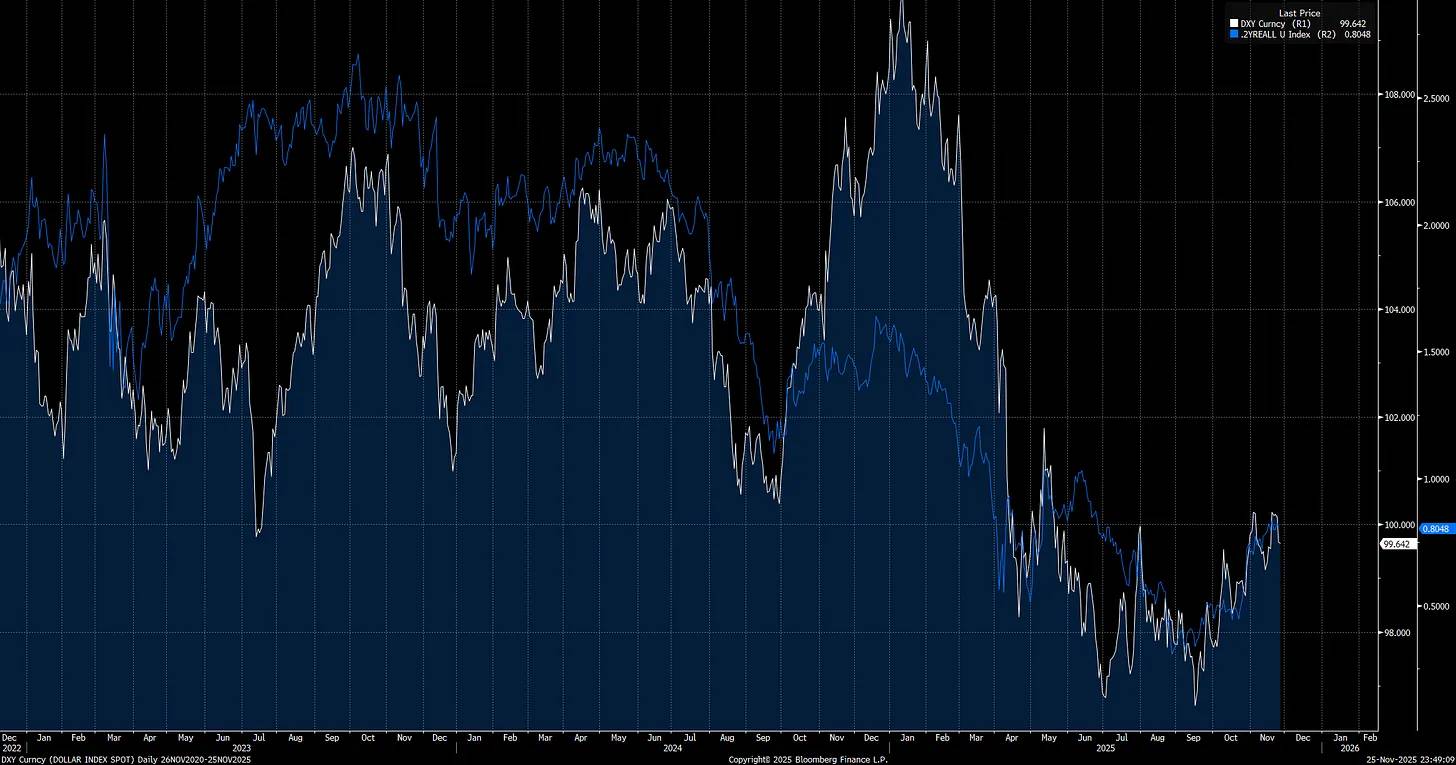

From the moment Trump took office (red arrow), the US Dollar Index (DXY) began to fall, and this is just the beginning.

Note that short-end real rates are one of the main drivers of the DXY, meaning monetary policy and Trump’s tariff policy are both key drivers of this trend.

Trump needs the Fed to take a more dovish stance on monetary policy, not only to stimulate the economy but also to weaken the dollar. This is one reason he appointed Steven Miran to the Fed Board, as Miran has a deep understanding of how global trade works.

What was the first thing Miran did after taking office? He placed his dot plot projections a full 100 basis points below those of other FOMC members. This is a clear signal: he is extremely dovish and is trying to guide other members toward a more accommodative stance.

Key Point:

There is a core dilemma here: the US is in a real economic conflict with China and must respond actively or risk losing strategic dominance. However, a weak dollar policy achieved through extremely loose monetary policy and aggressive trade negotiations is a double-edged sword. In the short term, it can boost domestic liquidity, but it also suppresses cross-border capital flows.

A weak dollar may cause foreign investors to reduce their exposure to US stocks as the dollar depreciates, as they need to adjust to new trade conditions and a changing FX environment. This puts the US on the edge: one path is to confront China’s economic aggression head-on, the other is to risk a major repricing of US equities due to dollar devaluation against major currencies.

New Fed Chair, Midterm Elections, and Trump’s “Grand Strategy”

We are witnessing the formation of a global imbalance directly linked to cross-border capital flows and currency. Since Trump took office, this imbalance has accelerated as he began to confront the biggest structural distortions in the system, including economic conflict with China. These dynamics are not theoretical—they are already reshaping markets and global trade. All of this is laying the groundwork for next year’s catalytic event: a new Fed Chair will take office during the midterm elections, and Trump will enter the final two years of his term, determined to leave a lasting mark on US history.

I believe Trump will push the Fed to adopt the most aggressive dovish monetary policy to achieve a weak dollar until inflation risks force a policy reversal. Most investors assume a dovish Fed is always good for stocks, but this assumption only holds when the economy is resilient. Once dovish policy triggers adjustments in cross-border capital positions, this logic collapses.

If you have followed my research, you will know that long-term rates always price in central bank policy mistakes. When the Fed cuts rates too aggressively, long-term yields rise, and the yield curve bear steepens to counter policy errors. The Fed’s current advantage is that inflation expectations (see chart: 2-year inflation swaps) have been falling for a month, shifting the risk balance and allowing them to take a dovish stance in the short term without triggering significant inflation pressure.

As inflation expectations fall, we have news about the new Fed Chair, who will take office next year and may be more aligned with Miran’s stance than with other Fed governors:

If the Fed adjusts the terminal rate (currently reflected in the eighth SOFR contract) to better match changes in inflation expectations, this will start to lower real rates and further weaken the dollar (since inflation risk has just declined, the Fed has room to do this).

We have already seen that the recent rise in real rates (white line) has slowed the dollar’s (blue line) decline, but this is creating greater imbalances, paving the way for further rate cuts, which are likely to push the dollar even lower.

If Trump wants to reverse global trade imbalances and compete with China in economic conflict and AI competition, he needs a significantly weaker dollar. Tariffs give him negotiating leverage to reach trade deals aligned with a weak dollar strategy while maintaining US dominance.

The problem is, Trump and Bessent must balance multiple challenges: avoiding politically destructive outcomes before the midterms, managing a Fed with several less dovish members, and hoping the weak dollar strategy does not trigger foreign investors to sell US stocks, widen credit spreads, and hit a fragile labor market. This combination could easily push the economy to the brink of recession.

The greatest risk is that current market valuations are at historic extremes, making equities more sensitive to liquidity changes than ever before. That’s why I believe we are approaching a major inflection point in the next 12 months. The potential catalysts for a stock market sell-off are rising sharply.

“What important truth do very few people agree with you on?”

The market is sleepwalking into a structural risk that is almost unpriced: a deliberately engineered dollar devaluation, which will turn what investors see as tailwinds into the main source of volatility over the next year. The complacency around a weak dollar is just like the complacency around mortgages before 2008, and that’s why a deliberate dollar devaluation will hit risk assets harder than investors expect.

I firmly believe this is the most overlooked and misunderstood risk in global markets. I have been actively building models and strategies around this single tail event to go massively short when a structural collapse truly occurs.

Timing the Macro Inflection Point

What I want to do now is directly link these ideas to specific signals that reveal when particular risks are rising, especially when cross-border capital flows begin to change the macro liquidity structure.

In the US stock market, positioning unwinds happen frequently, but understanding the underlying drivers determines the severity of selling pressure. If the adjustment is driven by cross-border capital flows, the market is more fragile and risk vigilance needs to be significantly heightened.

The chart below shows the main periods when cross-border capital positions began to exert greater selling pressure on US stocks. Monitoring this will be crucial:

Note that since the EURUSD rebound and call skew spike during the March market sell-off, the market has maintained a higher baseline level of call skew. This elevated baseline is almost certainly related to potential structural position risk in cross-border capital flows.

Whenever cross-border capital flows become a source of liquidity expansion or contraction, this is directly related to net flows through FX. Understanding the specific locations of foreign investors’ increases and decreases in US equities is crucial, as this will signal when risk is rising.

Factor, sector, and thematic underlying performance are key signals for understanding how capital flows operate in the system.

This is especially important for the AI theme, as more and more capital is disproportionately concentrated here:

To further explain the connections of these capital flows, I will release an interview with Jared Kubin for subscribers in the first week of December.

Main Signals of Cross-Border Sell-Offs Include

-

The dollar depreciates against major currency pairs, while cross-assetimplied volatilityrises.

-

Observing skew in major currency pairs will be key to confirming signals,

which can be monitored using the CVOL tool.

-

The dollar falls while the stock market also sells off.

Downward pressure in equities may be led by high beta stocks or thematic sectors, while low-quality stocks will suffer greater impact.

-

Cross-asset and cross-border correlations may approach 1.

Even small adjustments in the world’s largest imbalances can lead to high asset interlinkage. Monitoring other countries’ stock markets and factor performance will be crucial.

-

Final signal: Fed liquidity injections instead cause the dollar to fall further and intensify stock market selling pressure.

If policy-driven dollar devaluation triggers domestic stagflation pressure, this situation becomes even more dangerous.

See Brad Setser’s articles for reference.

Although gold and silver rose slightly during cross-border sell-offs earlier this year, they still sold off in a true market crash because they are cross-collateralized with the entire system. While holding gold and silver may have upside potential, they will not provide diversified returns when the VIX truly explodes. The only way to profit is through active trading, holding hedged positions, shorting the dollar, and going long volatility.

The biggest problem is: we are at a stage in the economic cycle where the real return on holding cash is becoming increasingly low. This systematically forces capital to move forward along the risk curve to establish net long positions before liquidity shifts. Timing this shift is crucial, because the risk of not holding equities in the credit cycle is as significant as the risk of not having hedges or holding cash in a bear market.

(I currently hold long positions in gold, silver, and equities because liquidity drivers still have upside potential.

I have detailed this for paid subscribers:

The Macro End Game

The core message is simple: global markets are ignoring the single most important risk of this cycle. The deliberate devaluation of the dollar, colliding with extreme cross-border imbalances and excessive valuations, is brewing a volatility event. This complacency is eerily similar to what we saw before 2008. While you can’t be certain about the future, you can analyze the present correctly. And current signals already show that pressure is gradually building beneath the surface.

Understanding these mechanisms is crucial because it tells you which signals to watch as risks approach, and these signals will become more pronounced. Awareness itself is an advantage. Most investors still assume a weaker dollar will automatically benefit the market. This assumption is dangerous and wrong today, just like the belief in 2007 that mortgages were “too safe.” This is the silent start of the macro end game, and global liquidity structure and currency dynamics will become the decisive drivers for every major asset class.

Currently, I remain bullish on equities, gold, and silver. But the storm is brewing. When my models begin to show a gradual rise in this risk, I will turn bearish on equities and immediately notify subscribers of this shift.

If 2008 taught us anything, it’s that warning signals can always be found if you know where to look. Monitor the right signals, understand the underlying dynamics, and when the tide turns, you’ll be ready.