In the development process of the crypto market, every once in a while, star projects emerge that can change the landscape. Nowadays, in the decentralized exchange (DEX) sector, Hyperliquid has firmly held the leading position, becoming the top choice for countless professional traders with its ultra-high-performance matching engine and ultimate user experience.

However, in the second half of 2025, a new force is rising rapidly, and that is Aster.

Figure 1: Aster platform homepage

In just a few months, Aster has achieved breakthrough growth in core metrics such as perpetual contract trading volume and TVL (Total Value Locked), and has been dubbed the "Hyperliquid killer" by the industry. Even more noteworthy, the endorsement effect of Binance founder CZ has caused the attention on this new project to skyrocket.

So, what exactly makes Aster a strong rival to Hyperliquid? Where are its advantages? How will the competitive landscape between the two evolve? This article will systematically dissect this new war in the Perps derivatives sector from multiple perspectives.

I. The Current State of the Perps Derivatives Sector

1. The Importance of Perpetual Contracts

Perpetual Futures are the most popular derivative tool in the crypto market. Unlike traditional futures, perpetual contracts have no expiration date, allowing traders to hold positions indefinitely while maintaining the contract price anchored to the spot price through a funding rate mechanism.

On centralized exchanges (CEX), the daily trading volume of perpetual contracts is often 3 to 5 times that of spot trading. For example, in 2024, Binance's daily futures trading volume once exceeded $60 billion, far surpassing spot trading volume.

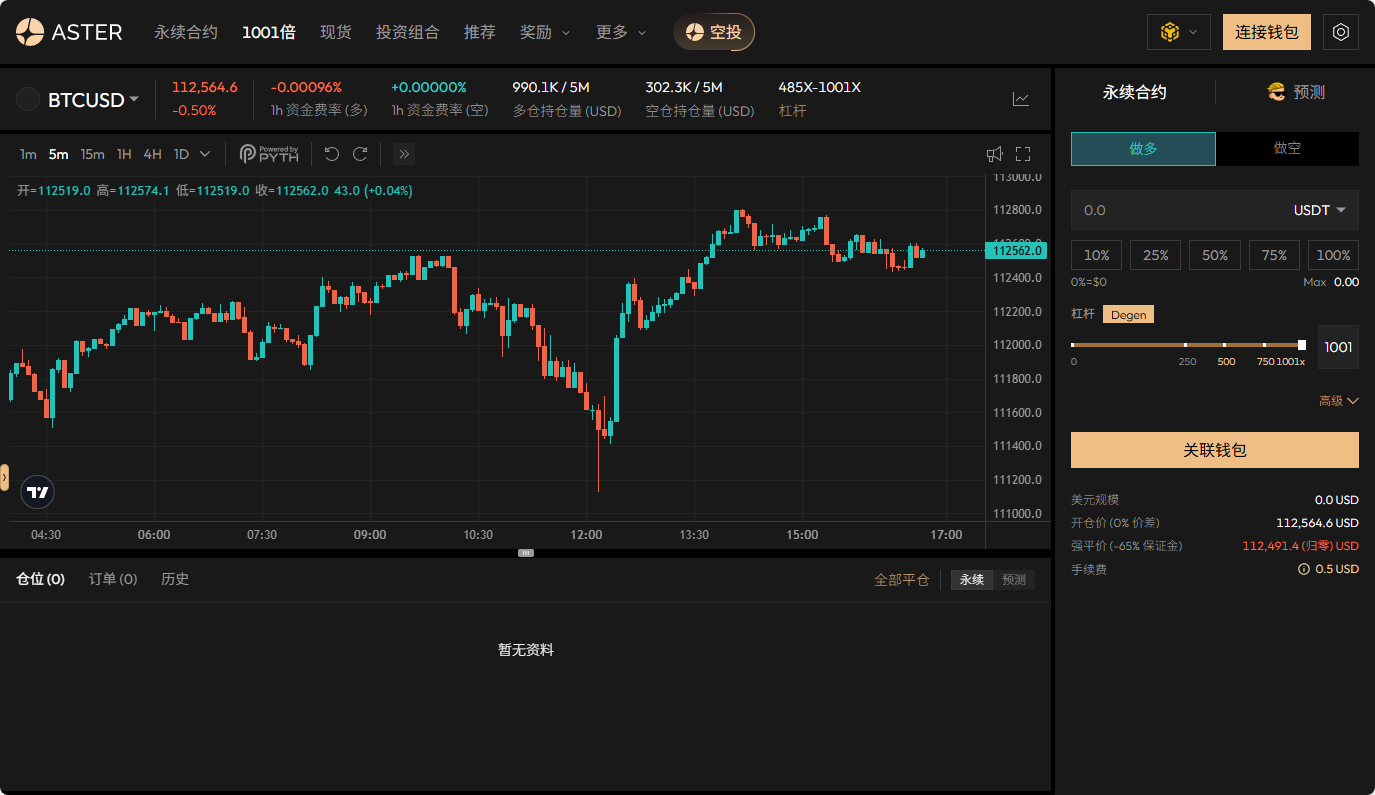

On decentralized exchanges (DEX), perpetual contracts are also seen as the most imaginative growth direction. DEXs can offer higher leverage than CEXs, especially for certain derivatives like perpetual contracts. Leverage on CEXs is usually subject to regulatory restrictions (such as the US SEC or EU MiCA), typically capped at 100x-125x, while the decentralized nature of DEXs allows platforms like Aster to offer up to 1001x leverage.

Figure 2: Aster platform 1001x leverage trading page

2. Hyperliquid's Leading Position

Hyperliquid's success lies in pioneering a new path: self-developed high-performance public chain + native matching engine. This means it no longer relies on existing public chains like Ethereum or BSC, but instead builds its own underlying network, achieving matching speed and smoothness close to that of CEXs.

Figure 3: Hyperliquid platform homepage

As of September 24, 2025: Hyperliquid's average daily trading volume remains around $1 billion, firmly ranking first among DEXs; open interest (OI) is $13.3 billion, with extremely deep liquidity; total users exceed 700,000, far surpassing other similar projects. Hyperliquid is thus known as the "on-chain Binance," and in the eyes of many, it has established a very high moat. (Data source: Defilama)

However, in the crypto world, nothing is set in stone. Every technological or model innovation can rewrite the landscape. In the second half of 2025, the sudden emergence of Aster is making this track once again unpredictable.

II. Aster's Differentiated Advantages

Rather than imitating Hyperliquid, Aster is blazing its own trail.

1. Innovation in Capital Efficiency

In derivatives DEXs like Hyperliquid, users mostly need to use stablecoins (USDT, USDC) as margin, and other assets (such as stETH, LSD, yield-bearing stablecoins) cannot be directly used as collateral, resulting in low capital utilization.

Aster, through a multi-asset collateral mechanism, has achieved the following innovations:

Supports staking assets (stETH, rETH, WBETH) as margin;

Supports yield-bearing stablecoins (such as sDAI, USDe) as margin;

Users can earn DeFi yields while using assets for leveraged trading.

For example: a user holds 1,000 stETH, which can earn an annualized yield of 3% when staked on Lido. On traditional derivatives DEXs, if he wants to open a contract, he must sell stETH for USDT, losing the staking yield. But on Aster, he can directly deposit stETH as margin, continue earning interest, and open BTC/ETH perpetual contracts.

This "dual utilization" greatly improves capital efficiency, especially suitable for DeFi veterans and large capital players.

2. Multi-Chain Expansion Strategy

Hyperliquid takes the single-chain extreme performance route, ensuring efficient matching through its self-developed chain. The advantage is speed and experience, but the downside is a closed ecosystem, requiring users to migrate assets to participate.

Aster, on the other hand, adopts multi-chain expansion:

Users can connect directly from Ethereum, BSC, Arbitrum, Optimism, etc.; through cross-chain bridges and liquidity aggregation, it ensures a seamless experience for users from different public chains.

This strategy has three benefits:

Lower migration barriers: users don't have to abandon their original asset ecosystems;

Introduce multi-source liquidity: assets from different chains can contribute to the liquidity pool;

Flexible expansion: can quickly support more emerging public chains in the future;

This gives Aster a broader user coverage than Hyperliquid.

3. Breakthroughs in Trading Volume and TVL

According to Defillama data, as of September 24, 2025: Aster's TVL is close to $1.8 billion, ranking among the top derivatives DEXs; 24-hour trading volume has exceeded $540 million. Although there is still a gap compared to Hyperliquid's $1 billion daily trading volume, as a newcomer established only a few months ago, this performance is quite impressive.

4. Optimization of User Experience

In product design, Aster strives to be close to CEXs:

Professional trading interface: K-line, order book, leverage multiples similar to Binance;

Hidden orders / iceberg orders: supports large capital users to place orders without affecting the order book.

Figure 4: Aster platform hidden order promotion page

Low-latency matching: the gap with CEXs has been greatly reduced; friendly UI/UX: lowers the learning curve for beginners.

This allows Aster to almost complete the leap from DEX to CEX in terms of user experience.

III. The Competitive Landscape Between Aster and Hyperliquid

One of the core reasons for Aster's rise is its sharp strategic contrast with Hyperliquid. To understand the competition between the two, we can look at three dimensions: core metrics, strategic direction, and user profiles.

1. Comparison of Core Metrics

Figure 5: Comparison of core metrics between Aster and Hyperliquid

From the data, Hyperliquid is still the absolute leader, ahead by several orders of magnitude in both trading volume and OI. But Aster's highlight is that its TVL has reached about 20% of Hyperliquid's, indicating strong capital attraction.

As a new platform that only appeared in 2025, being able to quickly break into the top ranks shows that its model does have differentiated competitiveness.

2. Comparison of User Profiles

Figure 6: Comparison of user profiles between Aster and Hyperliquid

In other words: Hyperliquid is more like the on-chain Binance; Aster is more like the on-chain "DeFi derivatives supermarket," emphasizing asset flexibility and capital efficiency.

3. Potential Substitution Effect

An important question is: will Aster steal users from Hyperliquid?

In the short term: professional traders will still stay on Hyperliquid, as it offers deeper liquidity and faster matching; but small and medium users, especially DeFi players, may prefer to "farm and trade" on Aster.

In the long term: if Aster can gradually catch up in depth and performance, it could very well become the first choice for mainstream users; once capital efficiency becomes the mainstream narrative, Hyperliquid's "performance advantage" may not be enough to lock in users. Therefore, calling Aster the "Hyperliquid killer" is not an exaggeration, as it could indeed create a substitution effect among certain user groups.

IV. CZ's Endorsement Effect

If Aster's product advantages are the internal cause, then CZ's endorsement is the external reason for its rapid popularity.

Figure 7, Figure 8: CZ reposts Aster tweets

As the founder of Binance, CZ's influence in the global crypto community is unparalleled. His tweets, comments, or even a single like can often trigger price fluctuations. In the industry discourse, CZ is also regarded as a "weathervane."

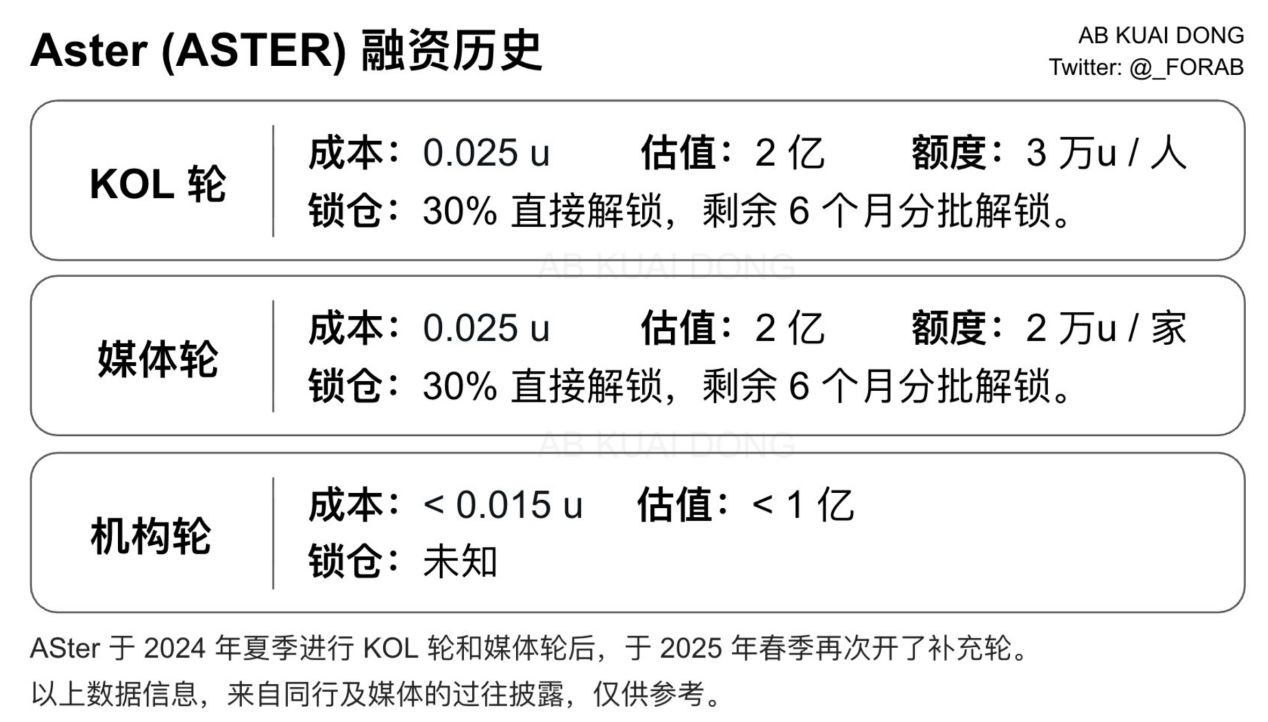

Figure 9: Aster financing history (reposted from X user @_FORAB)

Figure 10: Aster token price

Combining Aster's financing history and market performance, CZ's YZi Labs (formerly Binance Labs), as Aster's core investor and incubator, likely participated in Aster's early financing. Since the Aster token (ASTER) generation event (TGE) on September 17, 2025, its performance has been outstanding: the token price peaked at $2.3, and the current price is $2.2. If CZ's YZi Labs participated in Aster's institutional round (cost < $0.015), based on the current price, the investment return multiple has reached about 146 times.

Figure 11: Aster platform partners

V. Future Outlook

So, can Aster really become the ultimate challenger to Hyperliquid?

The decentralized derivatives market is still in a phase of rapid expansion, far from a "winner-takes-all" saturation state, and can accommodate the coexistence of multiple leading platforms. In this context, Aster benefits from the industry's strong demand for "capital efficiency"—as liquidity competition intensifies, users increasingly prefer platforms that can efficiently activate funds; it also enjoys continued support from CZ's influence and resources, further expanding its growth potential.

However, Aster also faces real challenges: there is still an order-of-magnitude gap with Hyperliquid in trading volume, open interest (OI), and user base; as a new platform, it still needs to withstand the market's test of security and stability over a longer cycle; whether it can transition from short-term explosive growth to long-term steady development is also a key test for the team. As for the future landscape, there are multiple possibilities: perhaps Hyperliquid and Aster will form a "dual hero" situation, coexisting with differentiated appeal to different user groups; if Aster's capital efficiency model is more favored by the market, it may even overtake Hyperliquid in trading volume; or new competitors may emerge, together shaping a multipolar competitive industry landscape.

Conclusion

In the DeFi world, there is no eternal overlord. Hyperliquid has proven itself with ultimate performance, while Aster has broken through with capital efficiency and a multi-chain strategy.

With CZ's endorsement, Aster has been given higher expectations and attention. Whether it will become the true "Hyperliquid killer" depends on whether it can maintain rapid growth over the next year and establish itself in terms of security and user trust.

What is certain is that Aster has successfully entered the market spotlight. The next chapter will not only belong to it, but will also determine the next phase of the decentralized derivatives sector.