From crypto to finance, and from finance to crypto

Cryptography, fintech, and AI are converging to form a new financial operating system.

Crypto, fintech, and AI are converging to form a new financial operating system.

Written by: 0xJeff

Translated by: AididiaoJP

Blockchain is a permissionless global rail where people can hold, transfer, buy, lend/borrow, and utilize their assets in any way they want, anywhere in the world.

Self-custody of funds means you still hold your own money even when interacting with services or applications.

This is the opposite of the traditional financial system, where banks (physical or digital) custody user funds and provide banking services to users.

The liquid nature of blockchain rails makes it a perfect setup for institutions seeking to move capital, enterprises looking to expand payment rails via stablecoins, or retail users seeking to invest/optimize their assets.

In this article, we will explore the shift from DeFi to fintech and Web2/Web3, the role of AI, transformations within the industry, and the opportunities that arise as a result.

Let’s dive in.

Let me tell you about Grab’s fintech strategy. Grab is one of the most dominant ride-hailing or super app players in Southeast Asia.

Grab initially offered ride-hailing services in Malaysia, aiming to make taxis safer and more reliable. The platform became popular in Malaysia and expanded to the Philippines, Thailand, Singapore, and Vietnam.

Grab didn’t just build a taxi app; it established a trust platform in a region with limited infrastructure and fragmented transportation systems.

Grab then expanded its services to include private cars, motorcycles, food delivery, parcel delivery, and an in-app payment system (wallet). All services use the same app, drivers, and payment rails, forming a super app ecosystem.

Grab realized that the wallet/payment rail (GrabPay) is the payment infrastructure that binds everything together (users pay for rides and deliveries, store value, and transact with merchants; drivers and riders use it to store/spend; financial data and transaction behavior are captured).

The payment infrastructure became the foundation for Grab to collaborate with lending and insurance startups to offer financial products (microloans, insurance) to drivers.

Now, GrabPay has evolved into a major regional e-wallet with more integrations and financial services (more embedded finance, merchant loans, driver loans using in-app credit scoring, and partnerships with banks and telecoms to offer financial products).

Grab’s strategy:

- Build a trust platform with a large user base on both demand and supply sides (users, drivers, merchants/suppliers).

- Connect everything with payment rails/wallet infrastructure and capture financial and consumer data.

- Build embedded financial products for the user base based on this data.

- Grab is now a fintech company, embedding itself deeper into finance: savings, investment, insurance, BNPL (Buy Now Pay Later), and digital banking.

From ride-hailing and food delivery to fintech.

Crypto and Fintech

We are starting to see strategies similar to Grab’s emerging simultaneously in Web3 projects and Web2 companies, i.e., crypto is becoming fintech, and fintech is becoming more crypto-oriented.

Why?

The TAM (Total Addressable Market) for crypto (revenue generated from services/applications) is very small compared to fintech’s TAM, so it makes a lot of sense to bring crypto’s value propositions (DeFi, tokenization, stablecoins, lending/borrowing, yield) to a broader consumer base.

Traditional rails still have friction in investing, saving, and accessing banking services, and in many cases, users must trust service providers to hold their funds. Blockchain is the perfect solution to this problem.

2 Case Studies

EtherFi (Crypto ➔ Fintech)

@ether_fi started in 2023 during the @eigenlayer restaking season as a liquidity restaking provider, offering restaked ETH and composable DeFi vault strategies that deploy eETH, weETH, and stablecoins into DeFi strategies to maximize returns. The team focused on liquidity and composability of growth strategies.

In 2025, Etherfi announced it would pivot to offering bank-like services and fintech features, combining DeFi with everyday financial use cases: spending, saving, earning, connecting crypto and fiat, bill payments, and payroll services.

The feature enabling more mainstream adoption is the Visa cash card, which allows users to spend their crypto directly or use their crypto as collateral to borrow stablecoins for spending (without selling your assets). The card offers about 3% cashback, token incentives, Apple Pay/Google Pay, and its non-custodial nature has attracted a large user base and transaction volume to its platform (and their vault products), i.e., more people deposit funds into EtherFi vaults.

Etherfi is positioning itself as a digital bank, bringing DeFi value to ordinary, mainstream users. Who wouldn’t want to seamlessly borrow stablecoins to spend or earn around 10%+ interest on their stablecoins?

Stripe (Fintech ➔ Crypto)

@stripe started in 2010, providing simplified payment infrastructure for developers and online businesses. Stripe offers merchants clean APIs to accept payments, manage subscriptions, handle fraud, make payouts, and embed financial services (solving a lot of headaches for any merchant).

Over time, Stripe expanded into a full-stack financial infrastructure platform, offering modular APIs and products that allow any company to build, embed, and scale financial services without becoming a bank.

- Stripe Connect: Enables marketplaces to pay out to third-party sellers, drivers, and creators globally, handling complex KYC and compliance in the background.

- Stripe Billing: Automated subscription system/backbone for SaaS.

- Stripe Treasury: Embedded finance (store funds, banking services).

- Stripe Issuing: Instantly create and manage physical or virtual cards.

- Stripe Radar: Integrated machine learning-driven fraud detection.

Stripe is testing crypto rails and acquiring major infrastructure players, acquiring Bridge (stablecoin payment infrastructure), Privy (crypto wallet/onboarding infrastructure), and then announcing a full push to own its own blockchain by developing a payment-first L1 (Tempo).

Stripe is positioning itself as the foundational layer for next-generation global payments, unifying fiat, stablecoins, and on-chain rails under a single developer platform—programmable, borderless money.

What does all this mean?

Besides these two players, many more are trying to get a piece of the pie.

Essentially, this means DeFi and TradFi, Web2 rails and Web3 rails are converging, and blockchain is becoming the backbone infrastructure supporting the real-world economy.

DeFi TVL could grow 10x from $174 billion to $1.74 trillion in the next five years. The wealth management sector holds $140 trillion, and it seems very likely that about 1% will be allocated to DeFi.

Stablecoins may eventually power universal applications and platforms behind the scenes, while also providing yield to users.

Spot, perpetual contracts, and prediction markets are becoming more mainstream, as the value proposition of trading crypto, tokenized stocks, on-chain commodities, and any asset (events, politics, macro, Taylor Swift) is enormous. Every business will want to own these user bases.

Due to industry convergence, enterprise sales and strategies targeting ordinary retail users will become essential.

Crypto “projects” will need to become “startups.” Reduce the geek hype, increase professionalism + build trust.

Builders need to sell DeFi platforms to enterprises, integrate DeFi vault products into fintech apps or wealth management platforms. Enterprise sales teams are also needed, understanding how to sell to them; risk/compliance and security will be key in their decision-making process.

We are starting to see early examples of this, with crypto-native teams operating far beyond CT.

- @Polymarket received investment from the parent company of the New York Stock Exchange (bringing Polymarket’s valuation to $9 billion), expanding prediction markets to TradFi and laying the foundation for the entire prediction market industry.

- @flock_io collaborates with governments, banks, international institutions, and public companies to deliver privacy-preserving, domain-specific AI. Flock’s dedicated team is tackling traditional industries/capital markets.

- @pendle_fi is working to bring TradFi/Wall Street onto on-chain interest rate products—KYC-based, permissioned pools.

- @Mantle_Official launched UR Global Digital Bank, “the world’s first blockchain-based digital bank.” Unified multi-asset accounts (with Swiss-backed IBAN accounts), Mastercard debit cards with SWIFT, SEPA, SIC, and L1/L2, facilitating deposits/withdrawals, self-custody, and upcoming DeFi integrations (idle balance yield, Mantle native DeFi products).

- @useTria started as BestPath, an AI-optimized solver network that finds the best swap paths across EVM, SVM, and other VMs (integrated with Sentient, Talus, Polygon, and Arbitrum Orbit chains). Tria has expanded to offer digital banking/fintech services, starting with cash cards (users earn yield from assets and can spend altcoins directly).

Exchanges are building embedded finance within on-chain wallets, serving as the discovery layer for all things DeFi (and soon TradFi), such as OKX Wallet, Binance Wallet, etc.

More crypto teams are launching crypto cards.

It appears that @CelsiusNetwork was on the right track, achieving native yield for bitcoin, ETH, and stablecoins, offering services such as deposit yield, collateralized loans, payments, and debit cards. The vision was right, but it failed due to poor execution, risk management, and lack of transparency.

How does Web3 AI fit in?

To keep it simple, there are three main aspects:

- Getting tasks done

- Ensuring you can trust the AI that completes the task

- Finding talent to make AI complete the task

Getting Tasks Done

Since crypto is mainly about financial use cases, AI systems that enhance DeFi, prediction, and trading experiences are the primary use cases Web3 AI builders are working on.

- Trading agents, AI-driven dynamic DeFi strategies, personalized DeFi agents, such as @Cod3xOrg, @Almanak, @gizatechxyz

- Prediction AI/ML teams, forecasting asset prices, prediction outcomes, weather, etc., such as @sportstensor, @SynthdataCo, @sire_agent

AI and ML systems are built on existing crypto verticals (mainly DeFi), enabling better accessibility, reducing complexity, and improving yield and risk management.

Ensuring you can trust the AI that completes the task

You can’t blindly trust AI, just as you can’t trust anyone, nor can you trust the infrastructure and people behind the AI. So who do you trust?

Yourself. You verify everything.

This is where verifiable infrastructure comes in.

Ethereum’s ERC-8004 acts as the trust layer, i.e., AI’s passport + Google’s AP2 + Coinbase x402 act as the payment system/rails (stablecoins and traditional rails), enabling agents to transact with each other or with other Web2 services.

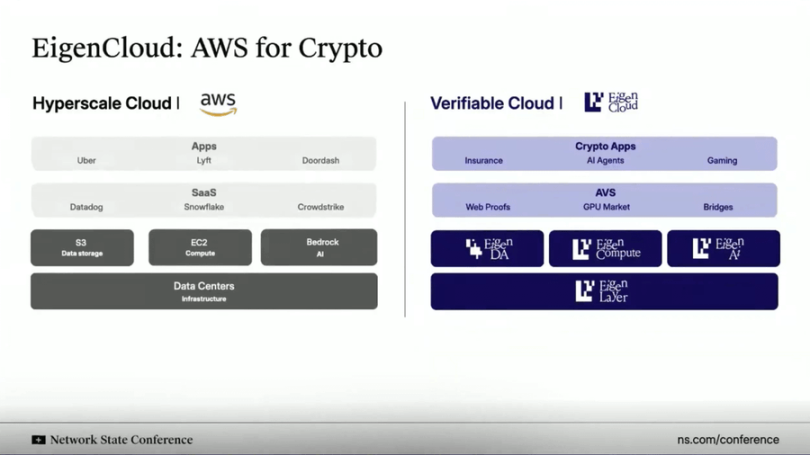

Just like AWS Cloud, @eigenlayer is providing verifiable cloud infrastructure for everything. Instead of hosting/running everything on centralized servers, Eigen supports off-chain computation while verifying results/inference on-chain.

This solution (EigenAI and EigenCompute) is perfect for AI agent/application use cases, such as trading agents and DeFi use cases.

Eigen has a primitive called deterministic inference, ensuring that LLMs produce the same output for the same input on repeated runs, i.e., ensuring they don’t hallucinate and become deterministic.

Just as restaked ETH is used to secure smart contracts, EIGEN is used to secure/prove AI agents/applications. Anyone can rerun the exact same inference to verify the reasoning and check if the output matches.

All this ensures:

(i) Trading agents don’t go rogue;

(ii) Recommendation engines in social media remain consistent/immutable every time;

(iii) Autonomous agents can safely hold funds because their reasoning can be audited/verified.

Finding Talent to Make AI Complete the Task

AI/ML engineers are among the most sought-after resources. If you’re really good, you’ll be poached by centralized frontier AI labs. If you’re extremely good, you’ll start your own.

Or you can choose to join a Darwinian AI ecosystem.

These ecosystems provide KPI-based incentives for “miners” and “trainers”—those who run AI or ML models to contribute/solve specific tasks. If your output is good and meets the target, you get rewarded handsomely.

Bittensor and @flock_io are two of the most well-known Darwinian AI ecosystems, where miners or trainers can earn six to seven-figure incentives annually based on their performance or the stake they hold within the ecosystem.

The goal of Darwinian AI ecosystems is to use incentives to attract talent, forming an active developer community contributing to specific tasks. The ultimate goal is to reach a stage where the revenue generated by output exceeds the cost of incentives.

Prediction models on Bittensor subnets outperform market benchmarks, or Flock delivers privacy-preserving, domain-specific AI use cases to large institutions and governments such as UNDP and Hong Kong.

Tying It All Together

Crypto, fintech, and AI are converging to form a new financial operating system.

At its core is the convergence of infrastructure.

Crypto rails are becoming the programmable, borderless settlement layer of the internet.

Fintech is providing the UX, compliance, and trust layer needed for mainstream adoption.

AI is becoming the decision-making and automation layer that optimizes liquidity, personalization, and user experience.

Stablecoins become the direct layer powering consumer applications, on-chain identity + verifiable computation underpin trust between AI agents/applications, traditional institutions and fintech integrate DeFi to unlock new yield opportunities, and millions of new users gain direct ownership, transparency, and global access to capital and intelligence.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Zcash Faces Vitalik Buterin’s Challenge: What Lies Ahead?

In Brief Vitalik Buterin warns Zcash against token-based governance. Zcash community is divided over future governance approach. ZEC Coin struggles with market negativity and volatile price movements.

70M$ inflows this week: Bitcoin ETFs rise again

BlackRock Downplays IBIT Outflows as Bitcoin ETF Market Shows Signs of Recovery