Is the reason for bitcoin's recent decline that Strategy is no longer "aggressively buying"?

Spot bitcoin ETFs, which have long been regarded as "automatic absorbers of new supply," are also showing similar signs of weakness.

Original Title: Why did Bitcoin's largest buyers suddenly stop accumulating?

Original Author: Oluwapelumi Adejumo, Crypto Slate

Translated by: Luffy, Foresight News

For most of 2025, Bitcoin's support level seemed unshakable, largely due to an unexpected alliance between corporate digital asset treasuries (DAT) and exchange-traded funds (ETF), which together formed a solid foundation of support.

Corporations purchased Bitcoin by issuing stocks and convertible bonds, while ETF inflows quietly absorbed the new supply. Together, these two forces built a strong demand base, helping Bitcoin withstand the pressures of a tightening financial environment.

Now, this foundation is beginning to weaken.

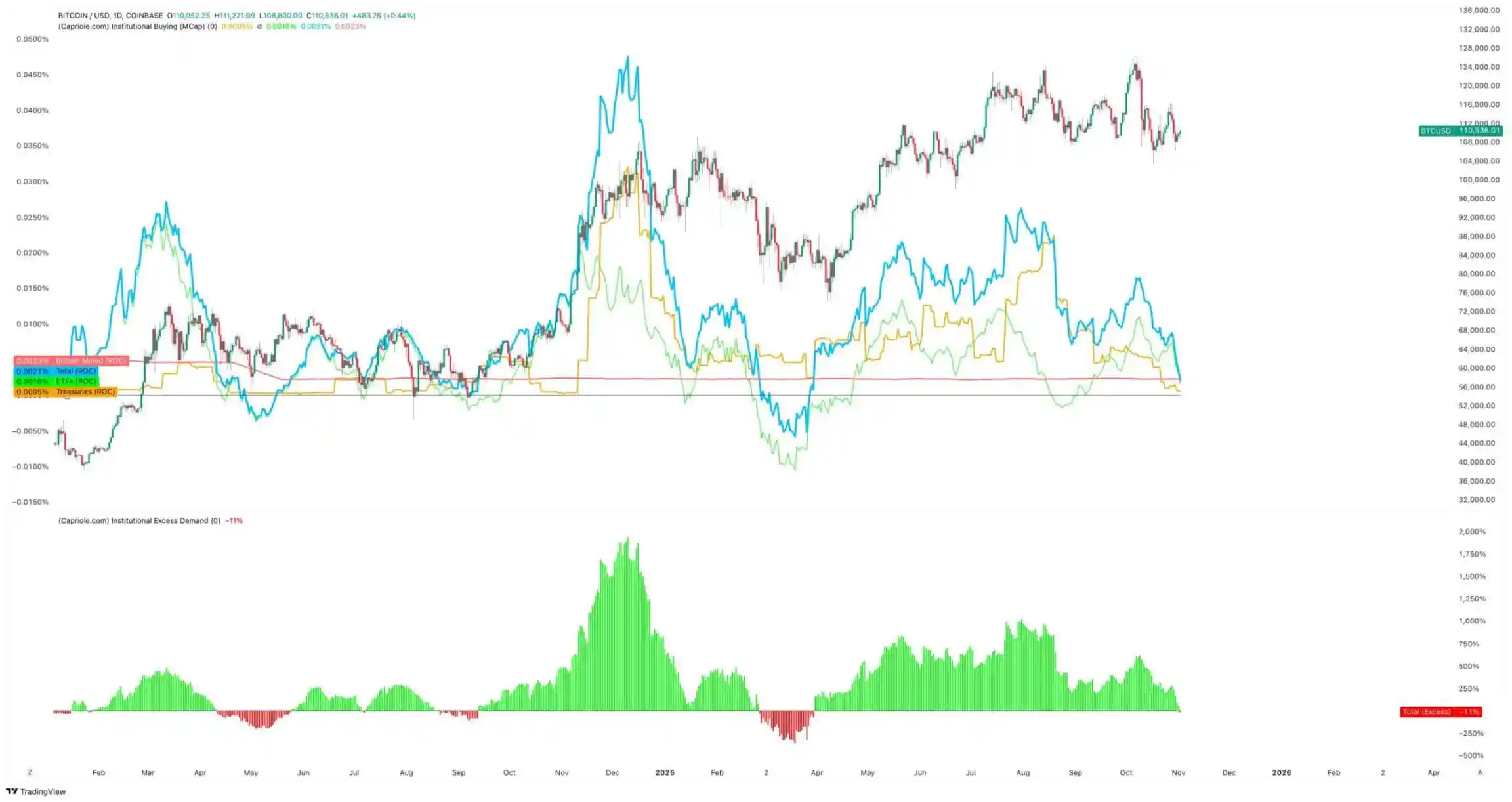

On November 3, Charles Edwards, founder of Capriole Investments, posted on X that his bullish outlook had diminished as institutional accumulation slowed.

He noted: "For the first time in seven months, net institutional buying has fallen below the daily mining supply. This is not a good sign."

Institutional Bitcoin buying volume, Source: Capriole Investments

Edwards stated that even when other assets outperform Bitcoin, this indicator has been the key reason for his continued optimism.

But as things stand, about 188 corporate treasuries hold significant Bitcoin positions, and many of these companies have relatively simple business models aside from their Bitcoin exposure.

Slowdown in Bitcoin Treasury Accumulation

No company better represents corporate Bitcoin trading than the recently renamed "Strategy" (formerly MicroStrategy).

This software maker, led by Michael Saylor, has transformed into a Bitcoin treasury company and currently holds over 674,000 Bitcoins, firmly establishing itself as the world's largest single corporate holder.

However, its buying pace has slowed significantly in recent months.

Strategy added only about 43,000 Bitcoins in the third quarter, marking its lowest quarterly purchase this year. Considering that some of its Bitcoin purchases during this period dropped to just a few hundred coins, this figure is not surprising.

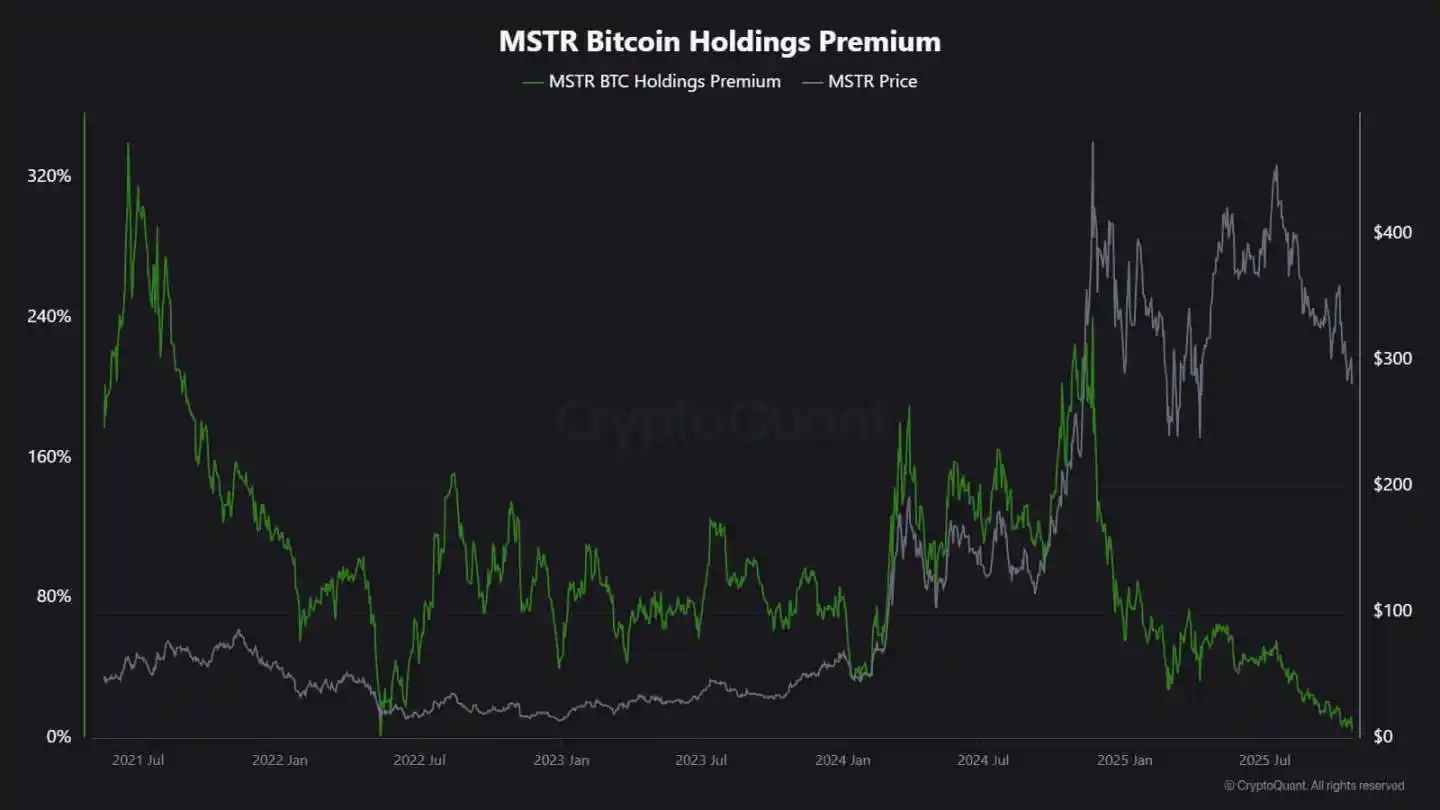

CryptoQuant analyst J.A. Maarturn explained that the slowdown in accumulation may be related to a decline in Strategy's net asset value (NAV).

He noted that investors used to pay a high "NAV premium" for each $1 of Bitcoin on Strategy's balance sheet, essentially allowing shareholders to share in Bitcoin's upside through leveraged exposure. But since mid-year, this premium has narrowed significantly.

With the valuation premium weakening, issuing new shares to buy Bitcoin no longer brings significant added value, and the motivation for corporate financing and accumulation has also decreased.

Maarturn pointed out: "Financing has become more difficult, and the stock issuance premium has dropped from 208% to 4%."

Strategy stock premium, Source: CryptoQuant

Meanwhile, the cooling trend in accumulation is not limited to Strategy.

Tokyo-listed Metaplanet once emulated this American pioneer, but after a sharp drop in its share price, it is now trading below the market value of its Bitcoin holdings.

In response, the company approved a stock buyback plan and introduced new financing guidelines to expand its Bitcoin treasury. This move demonstrates the company's confidence in its balance sheet, but also highlights waning investor enthusiasm for the "crypto treasury" business model.

In fact, the slowdown in Bitcoin treasury accumulation has led to some corporate mergers.

Last month, asset management firm Strive announced the acquisition of the smaller Bitcoin treasury company Semler Scientific. After the merger, these companies will hold nearly 11,000 Bitcoins.

These cases reflect structural constraints rather than a loss of conviction. When stock or convertible bond issuance can no longer command a market premium, capital inflows dry up and corporate accumulation naturally slows.

What About ETF Fund Flows?

Spot Bitcoin ETFs, long regarded as "automatic absorbers of new supply," have also shown signs of fatigue.

For most of 2025, these financial investment tools dominated net demand, with subscriptions consistently outpacing redemptions, especially as Bitcoin soared to all-time highs.

But by late October, their fund flows became unstable. Influenced by changes in interest rate expectations, portfolio managers adjusted positions, risk departments cut exposure, and some weekly fund flows turned negative. This volatility marks a new behavioral phase for Bitcoin ETFs.

The macro environment has tightened, hopes for rapid rate cuts have faded, and liquidity conditions have cooled. Nevertheless, demand for Bitcoin exposure remains strong, but has shifted from "steady inflows" to "pulsed inflows."

Data from SoSoValue vividly reflects this shift. In the first two weeks of October, crypto asset investment products attracted nearly $6 billion in inflows; but by the end of the month, as redemptions rose to over $2 billion, some of those inflows were erased.

Weekly Bitcoin ETF fund flows, Source: SoSoValue

This pattern suggests that Bitcoin ETFs have matured into true two-way markets. They still provide deep liquidity and institutional access, but are no longer one-way accumulation tools.

When macro signals fluctuate, ETF investors may exit as quickly as they enter.

Market Impact on Bitcoin

This shift does not necessarily mean Bitcoin is headed for a decline, but it does signal increased volatility. As the absorption capacity of corporations and ETFs weakens, Bitcoin's price action will be increasingly driven by short-term traders and macro sentiment.

Edwards believes that in this scenario, new catalysts—such as monetary easing, regulatory clarity, or a return of risk appetite in the stock market—could reignite institutional buying.

But for now, marginal buyers are more cautious, making price discovery more sensitive to global liquidity cycles.

The impact is mainly reflected in two aspects:

First, the structural buying that once served as a support level is weakening. During periods of insufficient absorption, intraday volatility may intensify due to a lack of stable buyers to dampen fluctuations. The April 2024 halving mechanically reduced new supply, but without sustained demand, scarcity alone cannot guarantee price appreciation.

Second, Bitcoin's correlation characteristics are changing. As balance sheet accumulation cools, the asset may once again track the overall liquidity cycle. Periods of rising real interest rates and a strengthening dollar may pressure prices, while a loose environment could see Bitcoin regain leadership during risk-on rallies.

Essentially, Bitcoin is re-entering a phase of macro reflexivity, behaving more like a high-beta risk asset than digital gold.

At the same time, none of this negates Bitcoin's long-term narrative as a scarce, programmable asset. On the contrary, it reflects the growing influence of institutional dynamics—institutions that once shielded Bitcoin from retail-driven volatility are now the very mechanisms tying it more closely to capital markets.

The coming months will test whether Bitcoin can maintain its store-of-value properties in the absence of automatic corporate and ETF inflows.

If history is any guide, Bitcoin tends to adapt. When one demand channel slows, another emerges—possibly from national reserves, fintech integration, or the return of retail investors during macro easing cycles.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin price gets $92K target as new buyers enter 'capitulation' mode

Full statement from the Reserve Bank of Australia: Interest rates remain unchanged, inflation expectations raised

The committee believes that caution should be maintained, and that outlook assessments should be continuously updated as data changes. There remains a high level of concern regarding the uncertainty of the outlook, regardless of its direction.