Why Does Bitcoin's Price Surge When the US Government Shuts Down?

Is the US Government Shutdown the Main Culprit Behind the Global Financial Market Decline?

The U.S. government shutdown has officially entered a record-breaking 36th day.

Over the past two days, global financial markets have plummeted. The Nasdaq, Bitcoin, tech stocks, Nikkei index, and even safe-haven assets like U.S. Treasuries and gold have not been spared.

Fear has gripped the markets, while Washington politicians continue to squabble over the budget. Is there a connection between the U.S. government shutdown and the global financial market downturn? The answer is emerging.

This is not a typical market correction but a liquidity crisis triggered by the government shutdown. With fiscal expenditures frozen, hundreds of billions of dollars are trapped in the Treasury's accounts, unable to flow into the market, severing the financial system's circulatory system.

The Treasury's "Black Hole"

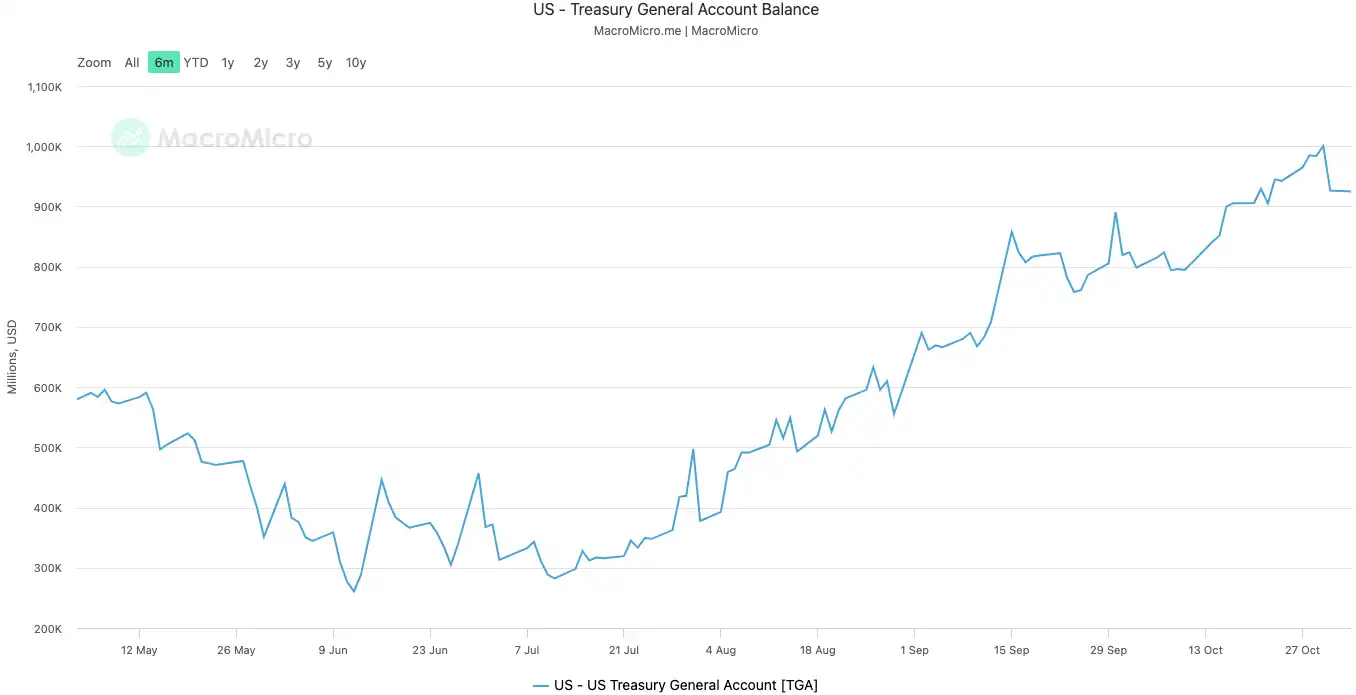

The U.S. Treasury's General Account, known as the TGA, can be understood as the U.S. government's central checking account at the Federal Reserve. All federal revenues, whether from taxes or issuing bonds, are deposited into this account.

And all government expenditures, from paying civil servant salaries to defense spending, are also disbursed from this account.

Under normal circumstances, the TGA acts as a fund's hub, maintaining a dynamic balance. The Treasury receives money and then quickly spends it, with funds flowing into the private financial system, becoming bank reserves, providing liquidity to the market.

The government shutdown has disrupted this cycle. While the Treasury continues to receive money through taxes and bond issuance, the TGA's balance keeps growing. However, since Congress has not approved a budget, most government agencies are closed, and the Treasury is unable to spend as planned. The TGA has turned into a financial black hole that only takes in but does not give out.

Since the shutdown began on October 10, 2025, the TGA's balance has ballooned from around $800 billion to over $1 trillion by October 30. In just 20 days, over $200 billion of funds have been sucked out of the market and locked in the Fed's vault.

U.S. Government's TGA Balance | Source: MicroMacro

Some analyses indicate that the government shutdown has withdrawn nearly $700 billion in liquidity from the market in one month. This effect is akin to the Fed conducting multiple rounds of rate hikes or accelerating quantitative tightening.

When the reserve of the banking system was heavily siphoned by the TGA, both the ability and willingness of banks to lend plummeted, causing a significant increase in the market's funding cost.

Those most sensitive to liquidity always feel the chill first. The cryptocurrency market crashed close to $20 billion in liquidations on the second day of the shutdown on October 11(UTC+8). This week, tech stocks also teetered, with the Nasdaq falling 1.7% on Tuesday, plummeting after Meta and Microsoft earnings reports.

The global financial market downturn is the most tangible manifestation of this stealth tightening.

The System is "Running a Fever"

The TGA was the "cause" of the liquidity crisis, and the skyrocketing overnight repo rate is the most direct symptom of the financial system "running a fever."

The overnight repo market is where banks lend short-term funds to each other, serving as the capillary of the entire financial system. Its rate is the most genuine indicator of the tautness of the interbank "money root." When liquidity is ample, interbank borrowing is easy, and rates are stable. However, when liquidity is drained, banks start running short of money and are willing to pay a higher price to borrow money overnight.

Two key indicators vividly illustrate how severe this fever is:

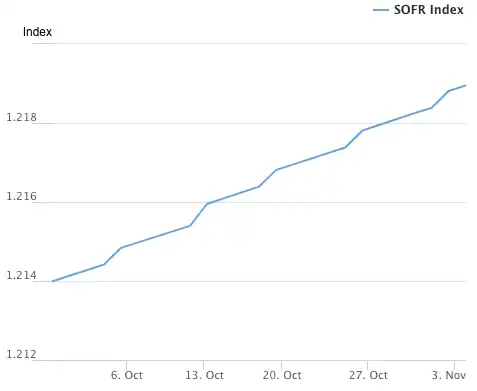

The first indicator is the Secured Overnight Financing Rate (SOFR). On October 31(UTC+8), SOFR surged to 4.22%, marking the largest single-day increase in a year.

This not only exceeded the upper limit of the Federal Reserve's target federal funds rate of 4.00% but was also 32 basis points higher than the effective federal funds rate, reaching the highest point since the market crisis of March 2020. The actual borrowing cost in the interbank market has spiraled out of control, far surpassing the central bank's policy rate.

Secured Overnight Financing Rate (SOFR) Index | Source: Federal Reserve Bank of New York

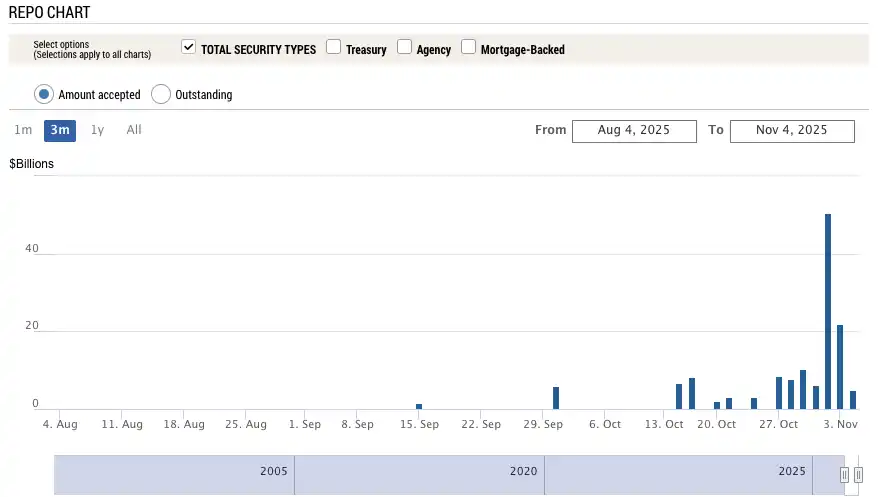

The second more astonishing indicator is the Federal Reserve's Standing Repo Facility (SRF) usage. The SRF is an emergency liquidity tool provided by the Federal Reserve to banks, allowing them to pledge high-grade securities for cash when they cannot borrow money in the market.

On October 31(UTC+8), SRF usage surged to $503.5 billion, hitting the highest level since the March 2020 pandemic crisis. The banking system has plunged into a severe dollar shortage, having to knock on the Federal Reserve's lender-of-last-resort window.

Spare Repurchase Facility (SRF) Usage | Source: Federal Reserve Bank of New York

The overheating of the financial system is now transmitting stress to the vulnerable segments of the real economy, triggering long-dormant debt landmines. The currently most dangerous areas are commercial real estate and auto loans.

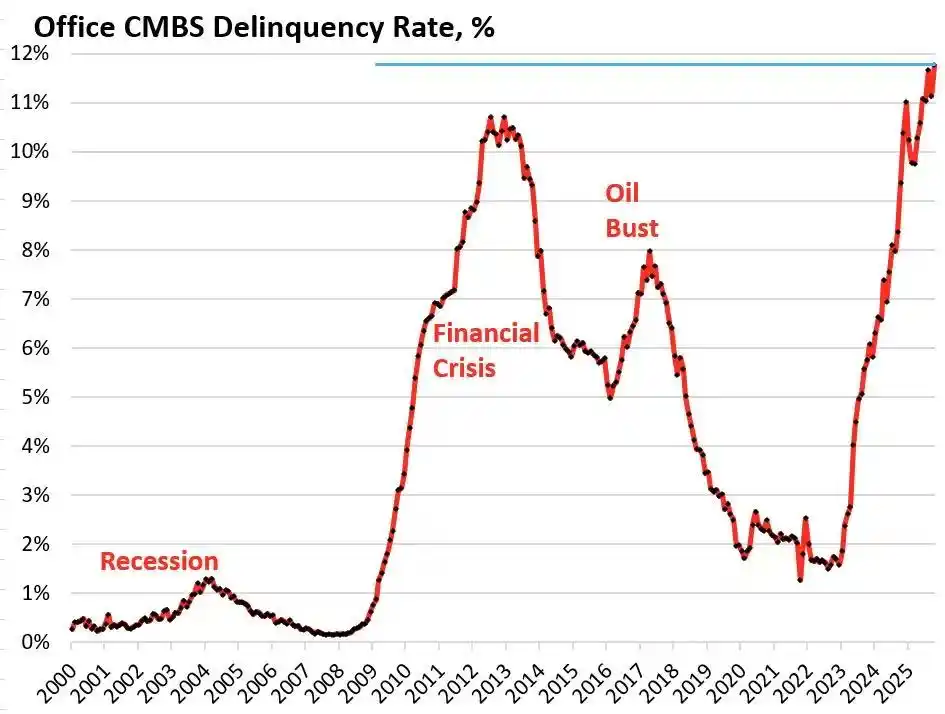

According to research firm Trepp, the default rate of US office building CMBS commercial real estate mortgage-backed securities reached 11.8% in October 2025(UTC+8), not only hitting a historic high but even surpassing the peak of 10.3% during the 2008 financial crisis. In just three years, this number has surged nearly 10 times from 1.8%.

US Office Building CMBS Commercial Real Estate Mortgage-Backed Securities Default Rate | Source: Wolf Street

The Bravern Office Commons in Bellevue, Washington, is a typical case. This office building, once fully leased by Microsoft, was valued at $6.05 billion in 2020. Now, with Microsoft's departure, the valuation has plummeted by 56% to $2.68 billion, and it has entered into default proceedings.

This most severe commercial real estate crisis since 2008 is spreading systemic risk throughout the financial system via regional banks, real estate investment trusts (REITs), and pension funds.

On the consumer side, the alarm bell for auto loans has also sounded. New car prices have soared to an average of over $50,000, and subprime borrowers are facing interest rates as high as 18-20%, heralding an impending wave of defaults. As of September 2025(UTC+8), the default rate for subprime auto loans has approached 10%, and the overall delinquency rate for auto loans has grown by over 50% in the past 15 years.

Meanwhile, surging energy prices are becoming another straw breaking the back of many households. In the backdrop of high inflation, the rise in electricity bills is particularly lethal. Since the beginning of 2025(UTC+8), the average American household electricity bill has risen by over 11%.

In Florida, 63-year-old wheelchair user Al Salvi's monthly electricity bill has reached nearly $500. "We now have to choose between paying the electricity bill and buying medication," he lamented in an interview with NPR in October(UTC+8).

This energy crisis, caused by multiple structural issues such as grid aging and AI-induced surge in power demand, compounded with interest rate and debt issues, is pushing ordinary American households to the brink of financial collapse.

From TGA's stealth tightening, to the overnight rate's systemic fever, to the soaring debt in commercial real estate and auto loans, a clear crisis transmission chain has emerged. The spark ignited by the unexpected Washington political deadlock is now setting off the long-existing structural weaknesses within the U.S. economy.

Worsening of the Labor Market

A deeper crisis is also brewing in the labor market, as the U.S. government shutdown not only drains the market's liquidity but also leaves the Federal Reserve devoid of its most crucial guidance for monetary policy: economic data.

Until the deadlock is resolved, key official economic data including the monthly jobs report and CPI inflation data will cease to be released. This means that at a critical juncture in the economy, the Fed's decisions will lack the most authoritative guidance.

In the absence of data, the market is forced to turn to alternative data from the private sector. The September ADP employment data released on October 1(UTC+8) (commonly known as "small nonfarm") showed a decrease of 32,000 jobs in the U.S. private sector, marking the first consecutive two months of negative growth in this data since the pandemic.

23-Year October - 25-Year September U.S. ADP Nonfarm Employment Population | Source: MicroMacro

In the last official employment data released before the government shutdown in August(UTC+8), only 22,000 new jobs were added, with historical data being significantly revised downwards by 911,000 jobs.

During the post-pandemic economic recovery period, monthly job additions in the U.S. typically range between 200,000 and 300,000. Now plummeting to 20,000 jobs, and even experiencing negative growth, this signals that the labor market has entered stagnation or even contraction. What is more concerning is the significant downward revision of historical data, indicating that the job market over the past year has been much weaker than officially reported.

Although the Federal Reserve cut interest rates as expected by 25 basis points during its meeting on October 31(UTC+8), the wording in the statement has shifted from the previous "strong labor market" to "the downside risks to employment have been rising." Atlanta Fed President Bostic went even further in his post-meeting speech, directly warning that employment risks have been escalating since August(UTC+8).

These expressions indicate that the Fed's concerns about the labor market are intensifying, a concern that is being confirmed by reality. Amazon announced layoffs of thousands, UPS is reducing management positions, and the once stable job market known as "no hire, no fire" is now turning to a wave of layoffs. After the large-scale layoffs in the tech industry from 2023 to 2024, hiring in 2025(UTC+8) has almost come to a standstill. Retail, logistics, financial services, and other industries have also reported layoff news.

Historical experience has repeatedly shown that a rapid increase in the unemployment rate is often a precursor to an economic recession. When the labor market shifts from prosperity to contraction, a wave of corporate layoffs begins to spread, consumer confidence collapses, and an economic recession often follows. If the current trend of deteriorating employment continues, the U.S. economy may face systemic risks more severe than a liquidity crisis -- an economic recession.

How Are Traders Viewing the Outlook?

How long will this liquidity crisis continue? Traders have differing opinions on this issue. They generally acknowledge the current state of liquidity tightening but hold different views on the macro trend for the next six months.

The pessimists represented by Mott Capital Management believe that the market is facing a liquidity shock comparable to the end of 2018. Bank reserves have fallen to dangerous levels, very similar to the conditions during the market turmoil triggered by the Fed's balance sheet reduction in 2018. As long as the government shutdown continues and the TGA continues to drain liquidity, the market's pain will not end. The only hope lies in the Treasury's Quarterly Refunding Announcement (QRA) on November 2(UTC+8). If the Treasury decides to lower the TGA's target balance, it could release over $150 billion of liquidity into the market. However, if the Treasury maintains or even raises the target, the market's winter will become even longer.

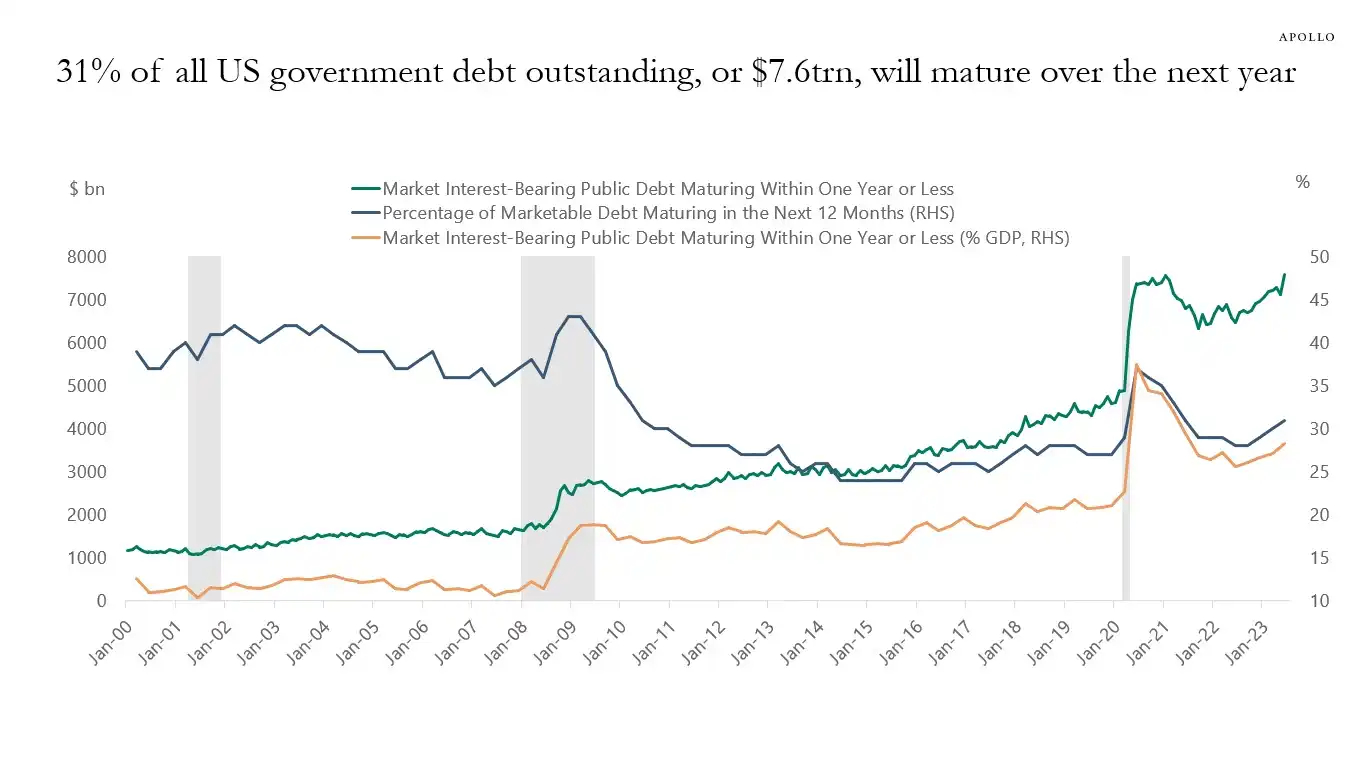

The optimists represented by renowned macro analyst Raoul Pal present an intriguing theory called the "Pain Window." He acknowledges that the current market is in a painful window of liquidity tightening but firmly believes that a liquidity flood will follow. In the next 12 months(UTC+8), the U.S. government has up to $10 trillion in debt rolling over, forcing it to ensure market stability and liquidity.

31% of the US government debt (about $7 trillion) will mature in the next year, along with new debt issuance, the total scale may reach $10 trillion|Image Source: Apollo Academy

Once the government shutdown ends, the pent-up hundreds of billions of dollars of fiscal spending will flood into the market like a deluge, and the Federal Reserve's quantitative tightening (QT) will also technically end, possibly even reversing.

To prepare for the 2026 midterm elections(UTC+8), the US government will stimulate the economy at all costs, including interest rate cuts, easing bank regulations, passing cryptocurrency bills, and more. Against the backdrop of continued liquidity expansion in China and Japan, the world will see a new round of monetary easing. The current pullback is just a shakeout in the bull market, and the real strategy should be to buy the dip.

Mainstream institutions like Goldman Sachs and Citigroup hold a relatively neutral view. They generally expect the government shutdown to end in the next one to two weeks(UTC+8). Once the deadlock is broken, the massive cash locked in the Treasury General Account (TGA) will be quickly released, thus alleviating market liquidity pressure. However, the long-term direction still depends on the Treasury Department's QRA announcement and the Fed's subsequent policies.

History seems to be repeating itself. Whether it's the 2018 taper tantrum or the repo crisis in September 2019(UTC+8), they all ended with the Fed's surrender and reinfusion of liquidity. This time, facing dual pressures of political deadlock and economic risks, policymakers seem to have once again come to a familiar crossroads.

In the short term, the fate of the market hangs on the whims of Washington politicians. But in the long run, the global economy seems to be deeply mired in a debt-monetization-bubble cycle from which it cannot extricate itself.

This crisis, unexpectedly triggered by the government shutdown, may only be the prelude to the next, larger-scale liquidity frenzy.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Microsoft Strikes $9.7B Deal With IREN as AI Demand Surges

XRP ETF: Nate Geraci predicts a launch within two weeks

Sequans Sells 970 Bitcoins, Unsettling the Markets

Crypto: Kaiko ranks XRP above Solana and Dogecoin in 2025