Has sector rotation in the crypto market really failed?

Even with the surge in BTC, early whales are either switching to ETFs or cashing out and exiting, with no further wealth spillover effect.

Even if BTC surges, early whales either rotate into ETFs or cash out and exit, with no further wealth spillover effect.

Written by: Ignas

Translated by: AididiaoJP, Foresight News

Why the classic crypto rotation pattern failed this cycle

BTC holders have already achieved excess returns, and early believers are taking profits. This is not panic selling, but a natural process of moving from concentrated to more distributed holdings.

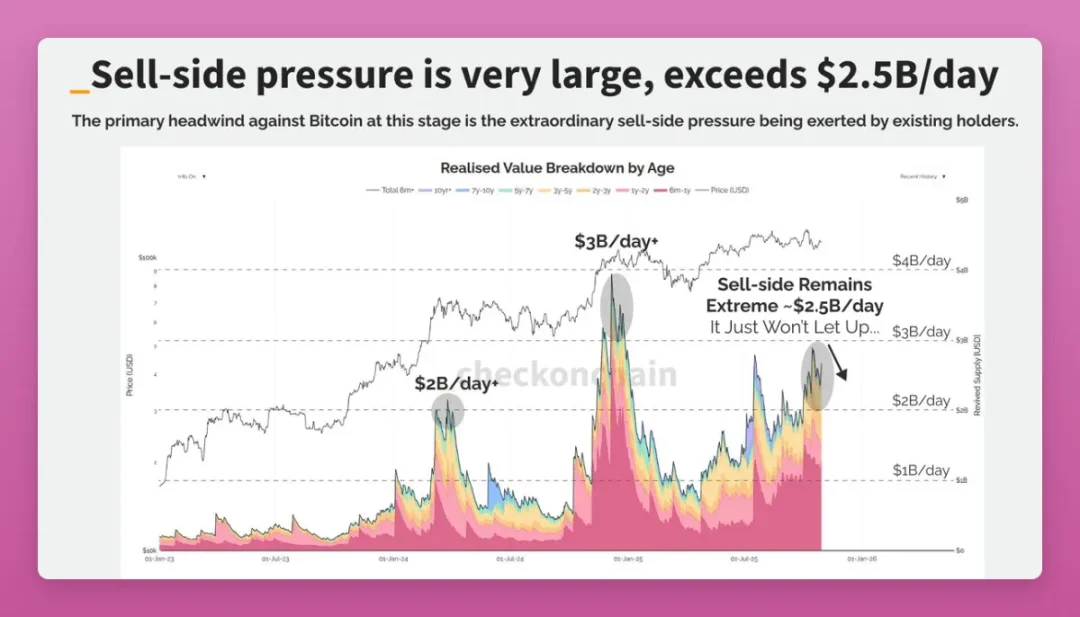

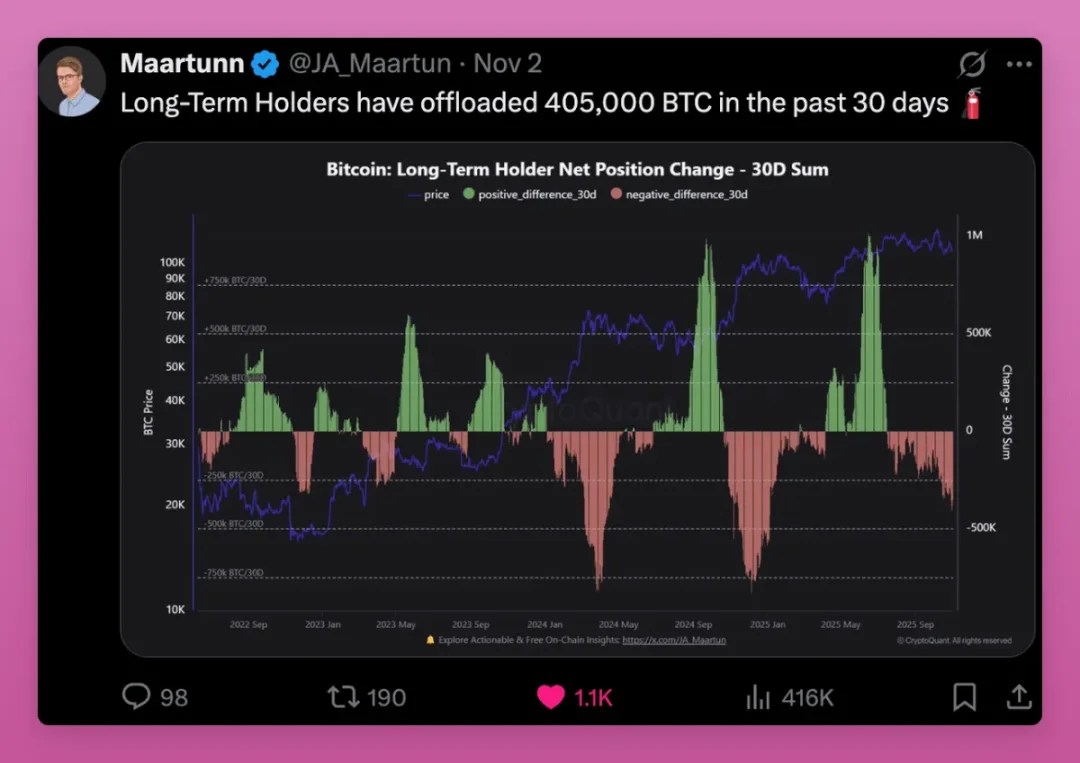

Among the many on-chain indicators, the most critical signal is whale selling behavior.

Long-term holders have sold 405,000 BTC in just 30 days, accounting for 1.9% of BTC's total supply.

Take Owen Gunden as an example:

This Bitcoin OG whale once traded large volumes on Mt. Gox, accumulated massive holdings, and served as a director at LedgerX. His associated wallet holds over 11,000 BTC, making him one of the largest individual holders on-chain.

Recently, his wallet has started transferring large amounts of BTC to Kraken. The act of transferring thousands of tokens in batches usually signals selling. On-chain analysts believe he may be preparing to liquidate holdings worth over 1.1 billions USD.

Although his Twitter account has been inactive since 2018, this move perfectly validates the "super rotation" theory. Some whales are rotating into ETFs for tax advantages or diversifying assets through selling.

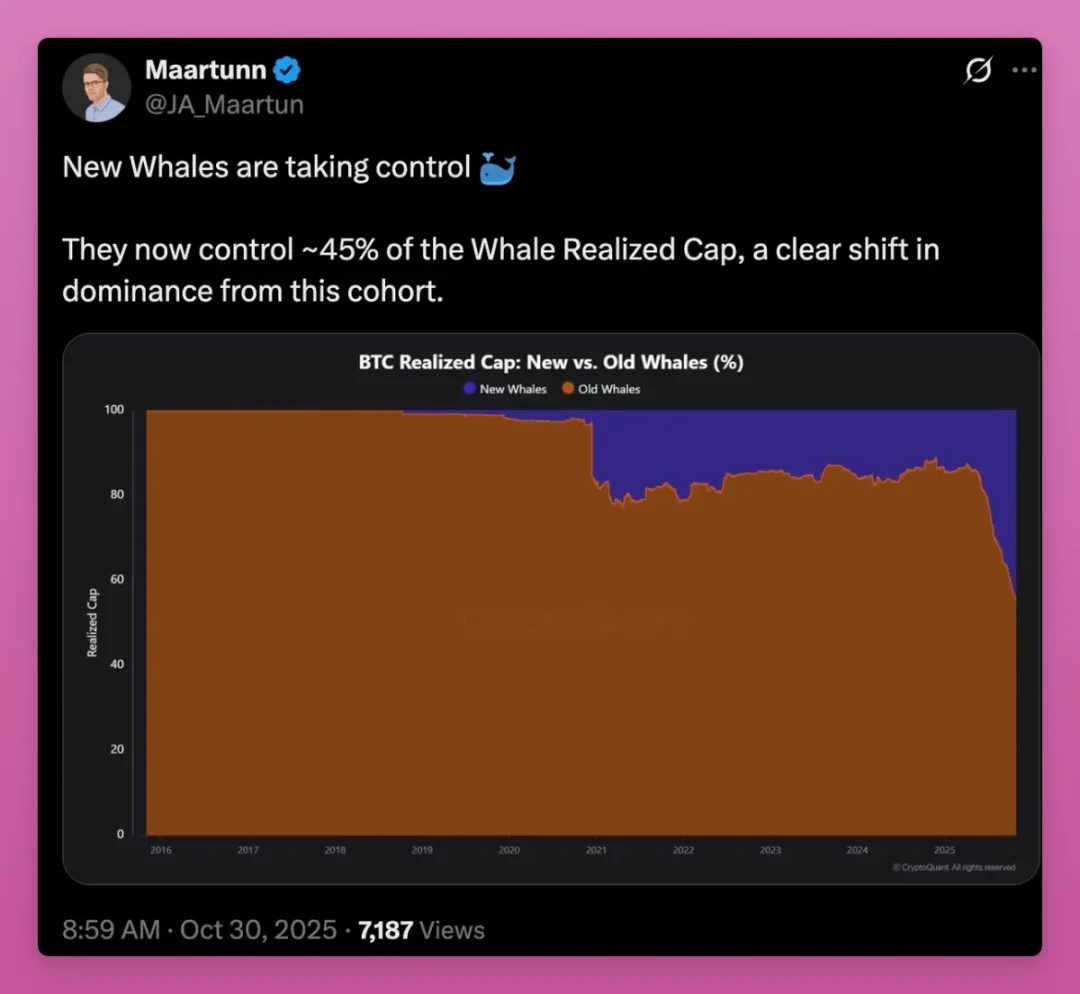

As tokens flow from OG holders to new buyers, unrealized profit prices continue to rise, and a new generation of whales is taking over market dominance.

The rising MVRV ratio confirms this trend, with the average cost basis shifting from early miners to ETF buyers and new institutions.

On the surface, this might seem bearish: whales have enjoyed huge long-term gains, while new whales are sitting on unrealized losses. The current average cost basis is as high as $108,000. If BTC remains weak, new whales may choose to sell.

But the rise in MVRV actually signals the diffusion of ownership and market maturation. Bitcoin is shifting from a few ultra-low-cost holders to a more distributed base with higher cost, which is essentially a bullish signal.

But what about altcoins?

The Ethereum Game

BTC has won, but what about ETH? Can we observe the same large-scale rotation pattern in ETH?

Although ETH's lagging price may be partly attributed to this, on the surface ETH is also successful: both have ETFs, DATs, and institutional attention (albeit of different natures). Data shows ETH is in a similar transitional phase, just earlier and more complex in process.

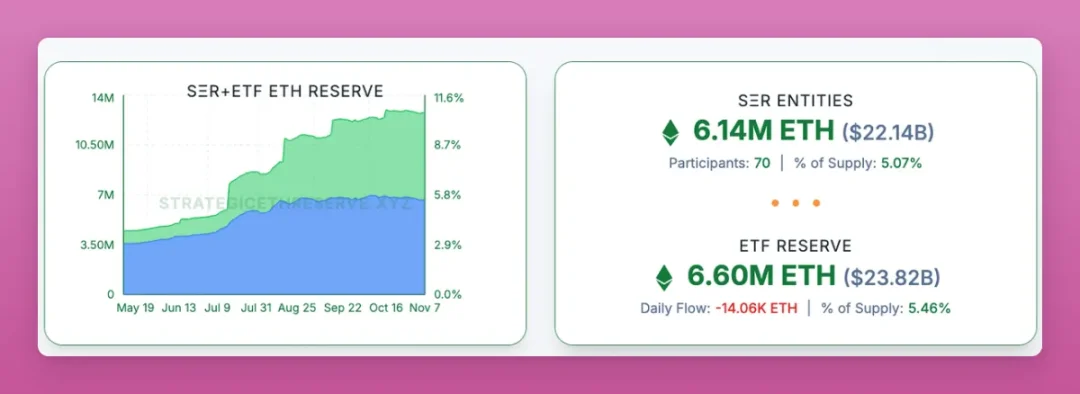

In fact, in one key dimension, ETH is quickly catching up to BTC: about 11% of ETH is held by DATs and ETFs…

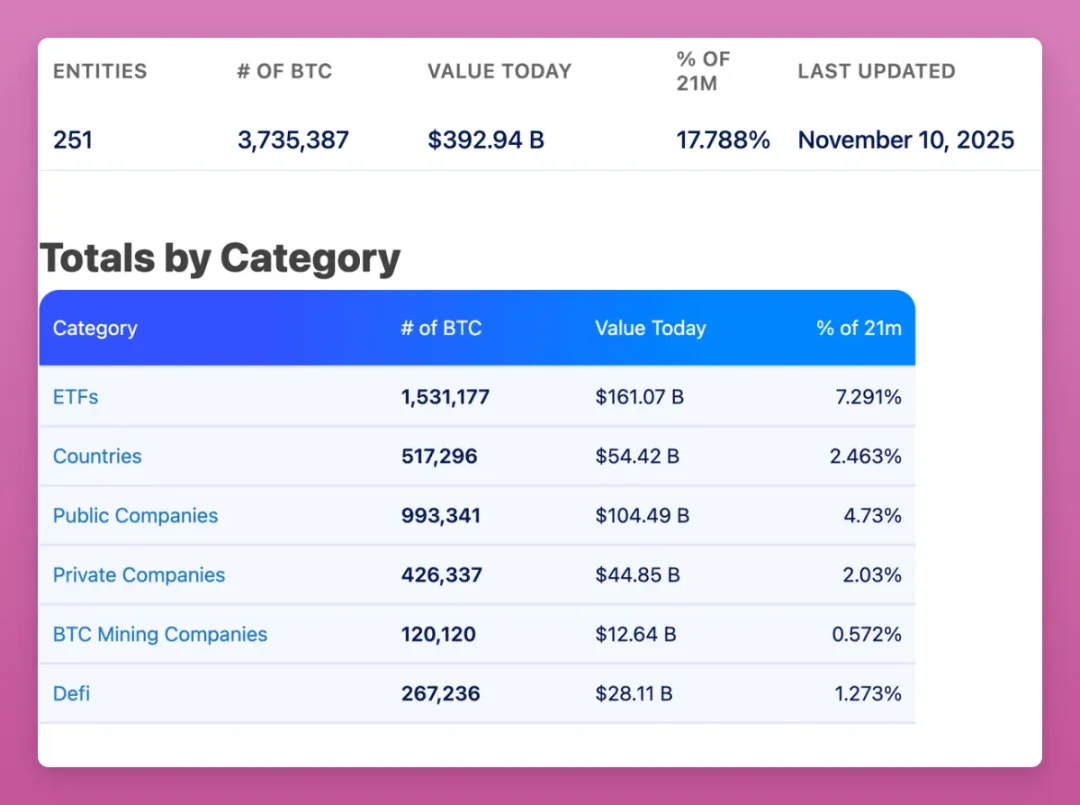

While 17.8% of BTC is held by spot ETFs and large treasuries. Considering Saylor's continued accumulation, ETH's catch-up speed is impressive.

We tried to verify whether ETH also has the phenomenon of old whales transferring to new whales, but due to ETH's account model (different from Bitcoin's UTXO model), it's difficult to obtain effective data.

The core difference is: ETH's transfer direction is retail → whales, while BTC is OG whales → new whales.

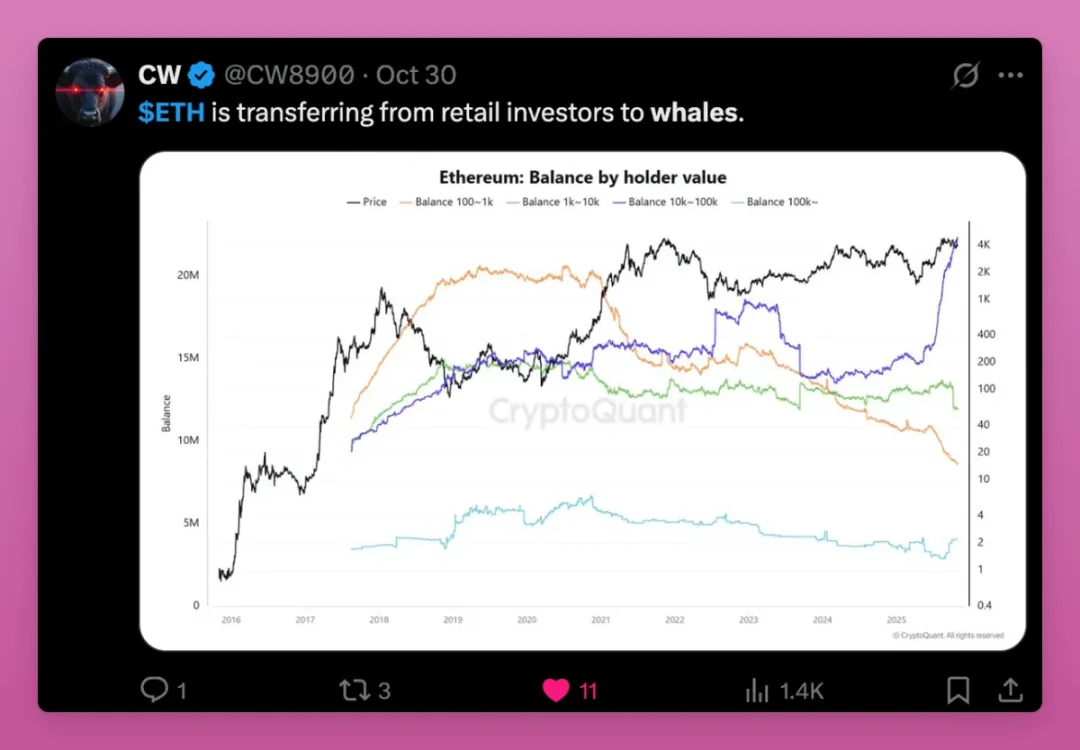

The chart below more intuitively shows the trend of ETH ownership shifting from retail to whales.

The realized price of large wallets (holding 100,000+ ETH) is rising rapidly, indicating new whales are building positions at higher costs, while retail continues to sell. The cost curves of different wallet types (orange, green, purple) are converging, meaning old cheap tokens have been transferred to new holders.

This kind of cost basis reset usually occurs at the end of an accumulation cycle and on the eve of a price breakout, structurally confirming that ETH supply is becoming more concentrated and solid.

ETH Outlook

This rotation logic holds because of:

- The popularity of stablecoins and asset tokenization

- The launch of staking ETFs

- The rollout of institutional-grade applications

These factors drive whales and funds to keep accumulating, while retail is losing faith in ETH as a "gas fee tool" and is being impacted by emerging public chains.

Whales view ETH as a yield-bearing asset and collateral, holding firmly for long-term on-chain returns. As BTC cements its dominance and ETH remains in a gray area, whales are seizing the institutional entry channel ahead of time.

The ETF+DAT combo makes ETH's holding structure more institutionalized, but whether this is tied to long-term growth remains uncertain. The biggest concern comes from the case of ETHZilla selling ETH to buy back stocks. While there's no need to panic, it has set a dangerous precedent.

Overall, ETH still fits the rotation theory, but because its holder structure is more complex, its use cases are richer (such as liquid staking concentrating tokens in a few large wallets), and on-chain activity is more frequent, the rotation pattern is less clear than Bitcoin's.

Solana's Advance

Analyzing Solana's position in this rotation is especially difficult (even identifying team wallets is a challenge), but there are still clues:

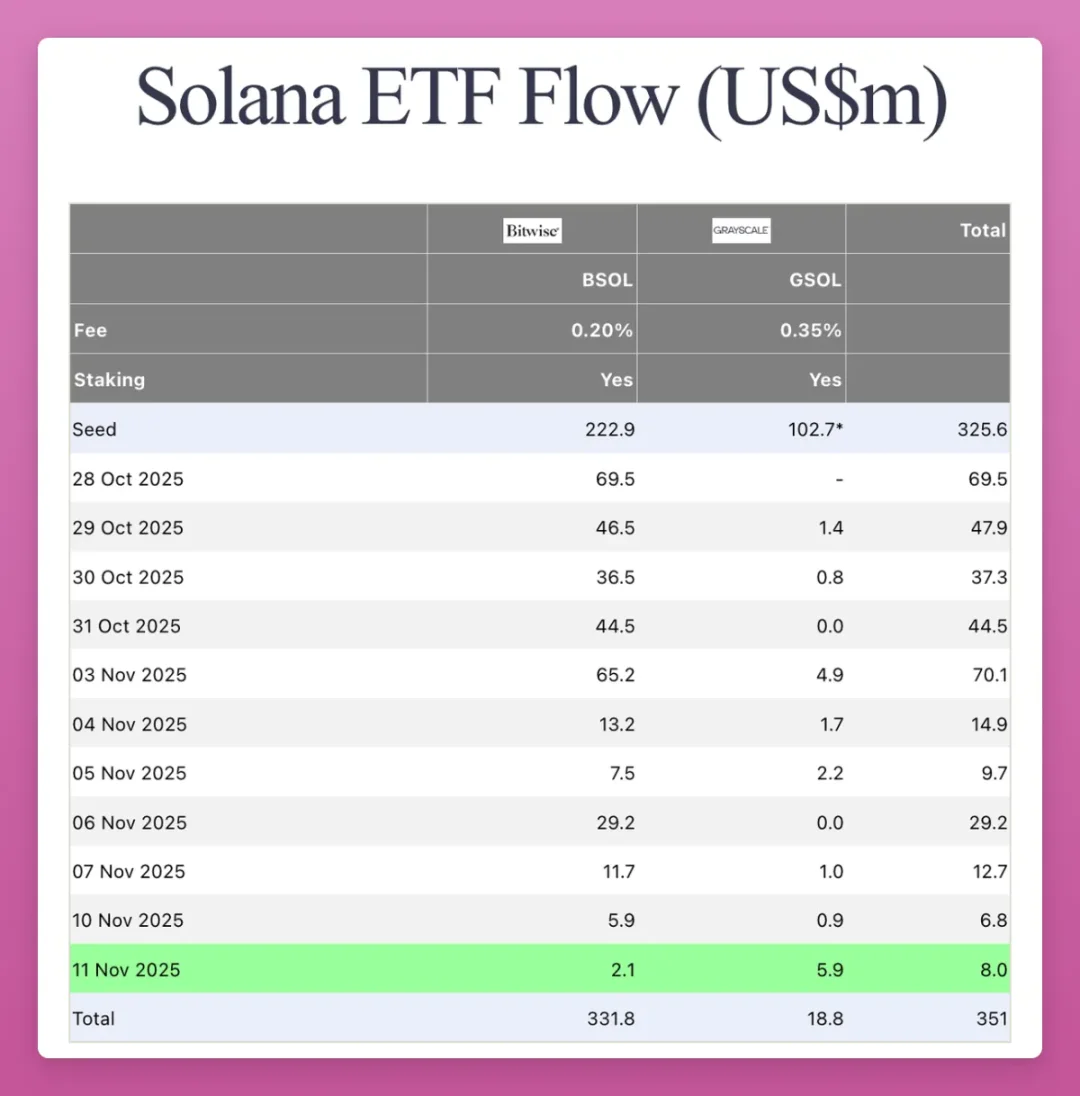

Solana is replicating Ethereum's institutionalization process. Last month, a US spot ETF quietly launched without much market buzz. Although the total size is only $351 million, it continues to see daily net inflows.

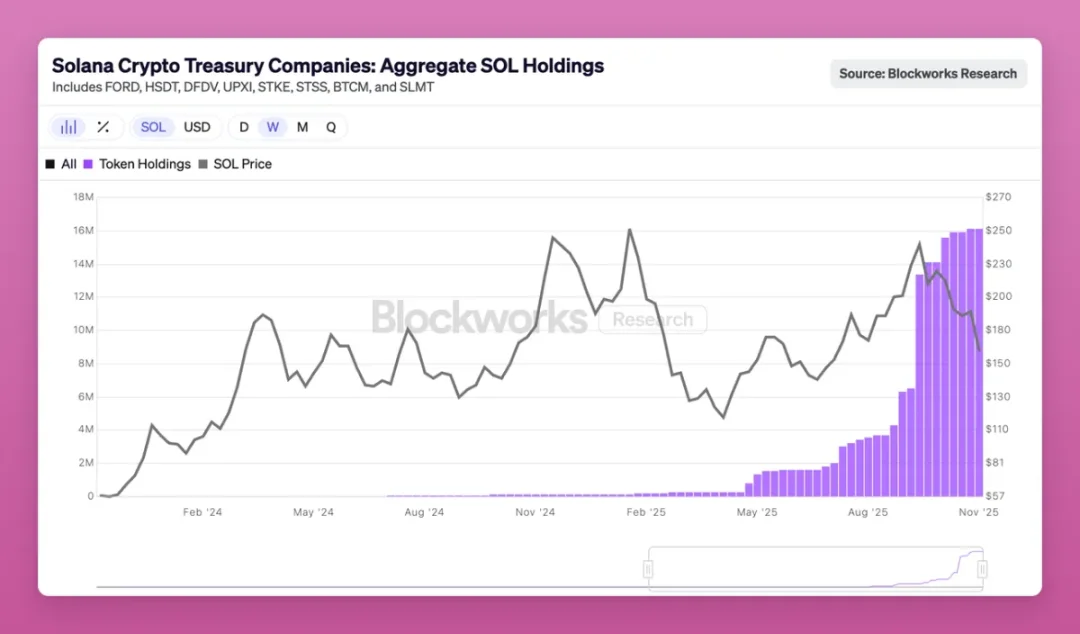

Early DAT positioning in SOL is also impressive:

2.9% of circulating SOL (worth $2.5 billion) is already held by DATs. At this point, Solana has built a traditional financial infrastructure similar to BTC/ETH (regulated funds + corporate treasuries), only the scale is still lagging.

Although on-chain data is messy and supply is still concentrated in early teams and VCs, tokens are steadily flowing to new institutional buyers via ETF/treasury channels. The large rotation has spread to Solana, just one cycle late.

Compared to BTC and ETH, whose rotations are nearing the end and price breakouts are imminent, SOL's trend forecast is actually more certain.

Future Direction

With BTC maturing first, ETH lagging behind, and SOL still needing time, where are we in the cycle?

Previous cycle logic was simple: BTC leads → ETH follows → wealth effect spreads to small-cap altcoins.

This cycle, however, is stuck at the BTC stage: even if BTC surges, early whales either rotate into ETFs or cash out and exit, with no further wealth spillover effect—only the trauma left by FTX and endless sideways movement remain.

Altcoins have given up competing with BTC for "currency" status, turning instead to compete on utility, yield, and speculation, but most will be eliminated.

Surviving sectors include:

- Public chains with real ecosystems: Ethereum, Solana, and a few promising projects

- Products that generate cash flow and value returns

- Assets with irreplaceable demand (such as ZEC)

- Infrastructure that captures fees and traffic

- Stablecoins and real-world asset tracks

- Ongoing crypto-native innovation

The rest will eventually be drowned out by noise.

The activation of Uniswap's fee switch is a milestone: although not the first, this move forces all DeFi protocols to share revenue with token holders. Currently, half of the top ten lending protocols have implemented revenue sharing.

DAOs are evolving into on-chain companies, and token value will depend on their ability to generate and redistribute revenue. This will also be the core battleground of the next rotation.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

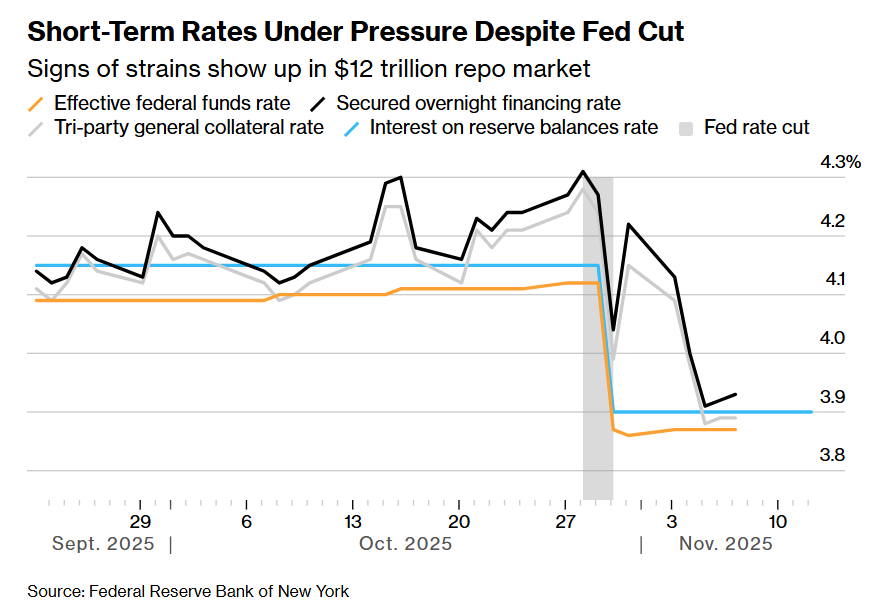

The 12 trillion financing market is in crisis! Institutions urge the Federal Reserve to step up rescue efforts

Wall Street financing costs are rising, highlighting signs of liquidity tightening. Although the Federal Reserve will stop quantitative tightening in December, institutions believe this is not enough and are calling on the Fed to resume bond purchases or increase short-term lending to ease the pressure.

Another Trump 2.0 era tragedy! The largest yen long position in nearly 40 years collapses

As the yen exchange rate hits a nine-month low, investors are pulling back from long positions. With a 300 basis point interest rate differential between the US and Japan, carry trades are dominating the market, putting the yen at further risk of depreciation.

Is a "cliff" in Russian oil production coming? IEA warns: US sanctions on Russia may have "far-reaching consequences"!

U.S. sanctions have dealt a heavy blow to Russia’s oil giants, and the IEA says this could have the most profound impact on the global oil market so far. Although Russian oil exports have not yet seen a significant decline, supply chain risks are spreading across borders.

Leading DEXs on Base and OP will merge and expand deployment to Arc and Ethereum

Uniswap's new proposal reduces LP earnings, while Aero integrates LPs into the entire protocol's cash flow.