K-shaped Divergence in Major Asset Pricing: The Subsequent Evolution of "Fiscal Risk Premium"

Southwest Securities believes that the current market is in a dangerous and fragmented period driven by "fiscal dominance," where traditional macro logic has failed, and both U.S. stocks and gold have become tools to hedge against fiat currency credit risk.

Southwest Securities believes that the current market is in a dangerous and divided moment driven by "fiscal dominance," where traditional macro logic has failed, and both US stocks and gold have become tools to hedge against fiat currency credit risk.

Written by: Ye Huiwen

Source: Wallstreetcn

The market is currently at an extremely dangerous and divided moment.

According to Chasing Wind Trading Desk, on December 4, research from Southwest Securities shows that since 2023, global major asset pricing has entered a brand new "fiscal dominance" stage, and the traditional macroeconomic transmission logic has basically failed. The market is showing a dramatic "K-shaped divergence": US stocks continue to rise despite employment pullbacks, gold has reached new highs in a high real interest rate environment, and a "fiscal risk premium" is generally embedded in the pricing of various assets.

The core risk does not come from the economic cycle itself, but from temporarily hidden fiscal pressures. Calculations show that the current system implies an interest rate gap as high as 600bp. Before macroeconomic control is lost, fiscal risk is temporarily hidden in the extreme rise of gold. In the future, the release and convergence of this risk tension will mainly rely on the marginal mitigation path of "gold falling, copper rising, and interest rates declining."

This means investors need to pay attention to the relative changes in gold, copper, and interest rates, using them as key indicators to measure the release of systemic risk. Asset prices have already shown a "dual consistency" structure: on one hand, US stocks and gold jointly hedge fiat currency credit risk; on the other hand, the mild divergence between stocks and bonds reflects the cost and dividends of fiscal expansion.

The Collapse of the Old Order: The Great Pricing Paradigm Shift After 2023

Since 2023, the market has completely broken the pricing logic of 2000-2022. Southwest Securities believes that traditional macro anchors have failed:

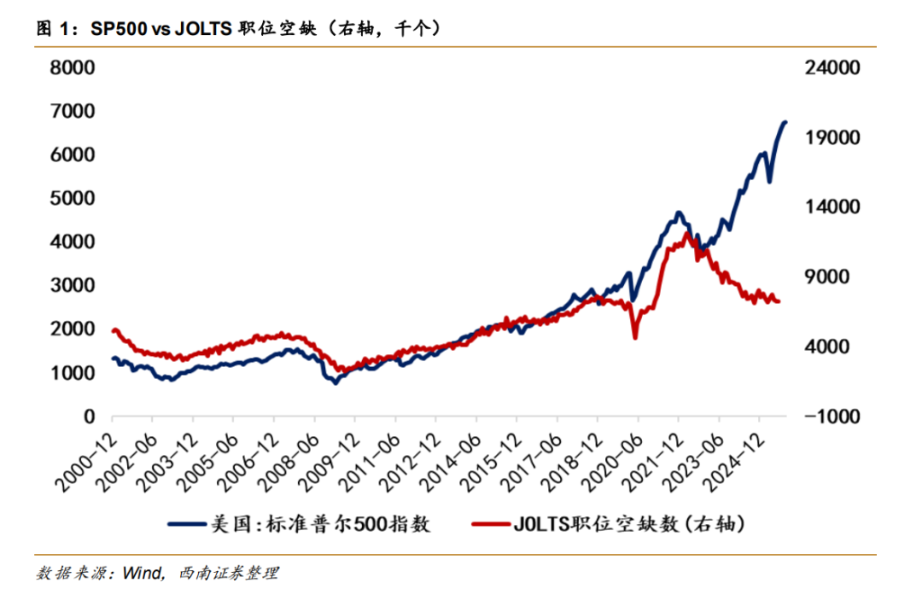

1. US stocks decouple from the economy: The S&P 500 index continues to hit new highs against the backdrop of a continuous decline in job openings (JOLTS), and the market has become desensitized to recession signals.

2. Gold decouples from interest rates: Gold completely ignores the suppression of high real interest rates and has moved independently, even diverging from TIPS (Treasury Inflation-Protected Securities).

3. Copper decouples from inflation: As a proxy variable for inflation expectations, copper prices no longer closely follow traditional inflation logic.

This divergence is not temporary market noise, but a fundamental change in underlying logic: the core anchor of market pricing has shifted from "economic fundamentals and monetary cycles" to "debt sustainability and fiscal risk." Now, every type of asset price has to factor in a high "fiscal risk premium."

Quantifying "Madness": Extreme Deviations Up to 400%

Data does not lie. Southwest Securities has precisely quantified the degree of current market distortion through regression backtesting of the old framework model:

US stocks and interest rates: The degree of deviation from the old model is astonishingly consistent, about 140%-170%.

Gold: Shows the most extreme "de-anchoring" feature, with a deviation exceeding 400%.

Copper: The deviation is relatively mild (about 44%).

This data reveals a core fact: in the early stage of fiscal dominance, the US fiscal risk premium is mainly priced through the extreme rise of gold, rather than directly impacting nominal interest rates. In other words, gold alone has taken on the responsibility of hedging the credit of the US denominated in fiat currency.

The Hidden 600bp Gap and the Interest Rate Model

Southwest Securities decomposes interest rates as a function of gold (implied TIPS) and copper (implied inflation expectations), and finds a surprising gap.

Model calculation: Since 2022, the extreme deviation between nominal interest rates and the "gold-copper implied rate" has reached as high as 660bp.

Mechanism analysis: For every $1 increase in gold, the implied interest rate falls by 0.2bp (fiscal risk premium rises); for every $1 increase in copper, only 0.0225bp of risk is marginally mitigated.

Conclusion: Even if the nominal interest rate on US Treasuries has not soared, in reality, fiscal risk has already exploded. The current level of interest rates is extremely high compared to the gold-denominated system. Mathematically, there are only three ways to ease this huge tension in the future: gold prices fall, copper prices rise, or nominal interest rates drop sharply.

The "Parallel Universe" in the Gold Coordinate System: US Stocks Have Become Gold-like

Southwest Securities points out that if you abandon the US dollar perspective and enter the "gold coordinate system," the world returns to "normal":

- US stocks return to rationality: US stocks priced in gold (stock-gold ratio) have not diverged from employment data (R2 reaches 77%), and the gap has significantly closed.

- Dual consistency: Both US stocks and gold have shown an extreme deviation of about 430% relative to the TIPS model. This proves that US stocks have essentially mutated into a "gold-like" asset to resist fiat currency depreciation, and the market is treating US stocks, especially tech stocks, as long-duration assets to hedge fiscal risk.

- The tacit understanding between stocks and bonds: The roughly 150% deviation at both ends is a form of profit distribution—interest rates bear the supply cost of fiscal expansion, while the stock market enjoys the nominal profit dividend of fiscal expansion.

Three Possible Evolutionary Paths for the Future

The implied fiscal risk premium will not disappear out of thin air; it will only shift between different assets. The possible macro paths for the future are as follows:

Mild recovery (short-term probability is higher): The market continues to remain in the illusion of the "gold coordinate system." As long as inflation expectations are suppressed, US stocks are supported by the AI narrative, and gold, stocks, and interest rates maintain a K-shaped divergence, waiting for copper prices to catch up and close the gap.

Inflation out of control (political shock): If a "crisis of affordability" leads to political pressure (such as a Trump administration being forced to implement tariff rebates or other forms of cash handouts), inflation will rise again. This will force fiscal risk to move from hidden to explicit—the result will be soaring interest rates, a depreciating US dollar, gold prices rising to a new level, and risk assets coming under pressure.

Recession liquidation (liquidity crisis): If employment data worsens and triggers a recession trade, it may replicate a global liquidity squeeze similar to the reversal of the yen carry trade. But under fiscal dominance, the safe-haven attribute of US Treasuries is marginally weakened, limiting the room for interest rates to fall, and at that time, both stocks and commodities may be hit.

In addition, the strength of the US dollar does not stem from the health of US finances, but because non-US economies (such as France and the UK) have exposed fiscal risks earlier—this is a structurally strong position in a "race to the bottom" game.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitcoin risks return to low $80K zone next as trader says dip 'makes sense'

Bitcoin ‘risk off’ signals fire despite traders’ view that sub-$100K BTC is a discount

Bitcoin’s end-of-year run to $100K heavily depends on Fed pivot outcomes

Ethereum’s major 2025 upgrade completed: a faster and cheaper mainnet has arrived

On December 4, Ethereum's second major upgrade of the year, Fusaka (corresponding to Epoch 411392), was officially activated on the Ethereum mainnet.