The Federal Reserve ends the year with a 25 basis point rate cut, causing significant market volatility. What lies ahead?

Shaw, Jinse Finance

On December 11, the Federal Reserve concluded the year with a rate cut, lowering the benchmark interest rate by 25 basis points to 3.50%-3.75%, marking the third consecutive meeting with a rate cut, in line with market expectations, with a total reduction of 75 basis points for the year. This FOMC statement indicated a conventional pace of rate cuts but exposed the largest internal division among voting policymakers in six years, suggesting a slowdown in actions next year and a possible pause in the near term. Subsequently, Federal Reserve Chair Jerome Powell's press conference was more dovish than expected. After the Fed's decision was announced, global markets reacted differently: U.S. stocks, short-term U.S. Treasuries, and gold rose intraday, the dollar fell, bitcoin fluctuated, briefly surging toward $94,500 before a significant pullback.

The Fed ended the year with a 25 basis point rate cut, but why are internal divisions still intensifying? The dot plot and Powell's press conference were more dovish than the market expected—what are the reasons behind this, and how should it be interpreted? Where will the market head in the future?

I. Fed Ends Year with Rate Cut, Uncertainty Remains for Next Year

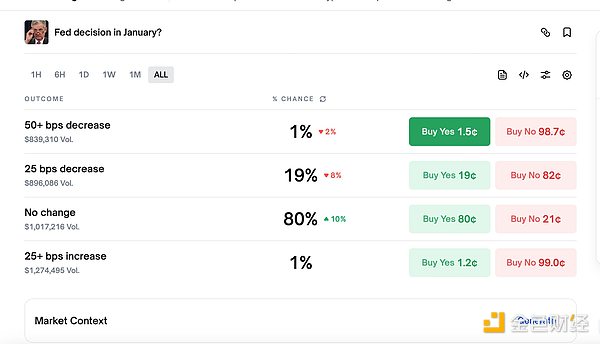

In the early hours today, the Federal Reserve announced its final rate decision of the year, lowering the benchmark rate by 25 basis points to 3.50%-3.75%, marking the third consecutive meeting with a rate cut, in line with market expectations, and totaling a 75 basis point reduction for the year. The subsequent FOMC statement showed that the Fed's rate decision faced three dissenting votes for the first time since 2019, exposing the largest internal division among voting policymakers in six years and suggesting a slowdown in actions next year, with a possible pause in the near term. U.S. interest rate futures indicate a 78% probability that the Fed will pause rate cuts at the January meeting next year, up from 70% before the FOMC decision. The latest CME "FedWatch" shows that the probability of a 25 basis point rate cut in January is 22.1%, while the probability of holding rates steady is 77.9%. By March next year, the probability of a cumulative 25 basis point cut is 40.7%, holding steady is 52%, and a cumulative 50 basis point cut is 7.4%. Prediction market Polymarket data shows that the market is betting on the Fed's January rate decision. After the announcement, the probability of holding rates steady in January has risen to 80%, while the probability of a 25 basis point cut has dropped to 19%.

After the rate decision was announced, global major asset markets reacted differently. U.S. stocks hit new intraday highs, with the S&P's gain narrowing from 1.2% to 0.7% near the end of Powell's press conference. The two-year U.S. Treasury yield fell 7.5 basis points intraday, spot gold rose 0.6%, hit a new intraday high, and approached $4,239. The dollar recorded its worst performance in nearly three months. The dollar index closed down 0.4%, the largest drop since September 16. Bitcoin briefly surged toward $94,500, hitting a new intraday high, but then experienced significant volatility and fell sharply, briefly dropping below $90,000.

The market had long expected a 25 basis point rate cut for the Fed's final rate decision of the year. However, the subsequent FOMC statement and dot plot revealed growing internal divisions within the Fed, causing the market to worry about the Fed's future policy path and casting doubt on whether rate cuts will continue next year.

II. FOMC Statement Highlights Intensifying Divisions, Dot Plot More Dovish Than Expected

This time, the Fed's FOMC statement announced that it would begin purchasing Treasury bills on December 12, buying $40 billion in Treasury bills over the next 30 days. The FOMC statement also announced that it would conduct standing overnight repurchase agreement operations at a rate of 3.75% and standing overnight reverse repurchase agreement operations at a rate of 3.50%, with a daily limit of $160 billion per counterparty. By purchasing Treasury bills and, if necessary, other U.S. Treasuries with a remaining maturity of no more than three years, the Fed will increase the securities holdings of the System Open Market Account to maintain an ample level of reserves. The statement noted that inflation has risen since the beginning of the year and remains elevated. Economic uncertainty remains high, and downside risks to employment have increased in recent months. In assessing the extent and timing of any further adjustments to the federal funds rate target range, the Committee will carefully evaluate the latest data, evolving economic outlook, and risk balance.

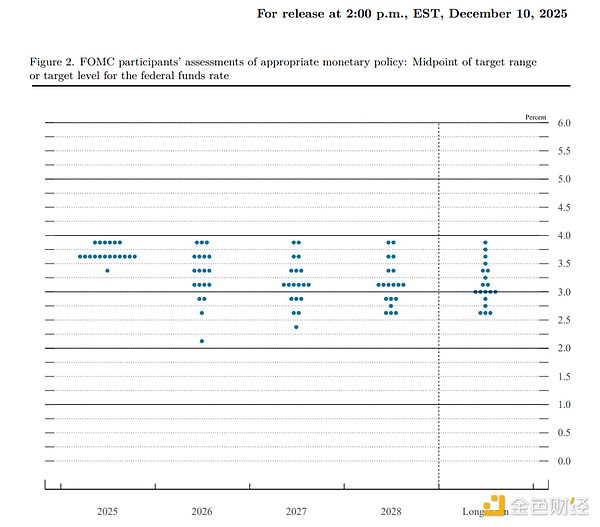

The dot plot released after the Fed meeting showed that among 19 officials, 7 believe there should be no rate cuts in 2026, 4 believe in a cumulative 25 basis point cut, 4 believe in a cumulative 50 basis point cut, 2 believe in a cumulative 75 basis point cut, 1 believes in a cumulative 100 basis point cut, and 1 believes in a cumulative 150 basis point cut.

The FOMC statement showed that this Fed rate decision faced three dissenting votes for the first time since 2019. Fed Governor Stephen I. Miran continued to advocate for a 50 basis point cut at this meeting; Kansas City Fed President Jeffrey Schmid and Chicago Fed President Austan Goolsbee advocated holding the federal funds rate target range steady; the other FOMC voting members supported the rate decision.

This Fed rate decision highlighted the largest internal division among voting policymakers in six years, suggesting a slowdown in actions next year and further fueling market concerns about the Fed's future policy path.

III. Powell's Press Conference More Dovish Than Expected, Intends to Finish His Term Steadily

Fed Chair Jerome Powell subsequently explained the rate cut decision and economic conditions at a press conference and answered reporters' questions. Powell stated that current data indicate the outlook is unchanged. The labor market appears to be gradually cooling, inflation remains elevated, consumer spending is still robust, and data show the economy is expanding at a moderate pace. Most long-term inflation expectations are consistent with the 2% target. If tariffs are removed, the inflation rate will be at the lower end of the 2% range. The Fed is committed to achieving the 2% inflation target, but the labor market is also under pressure. Powell said that the upward revision of the 2026 growth forecast partly reflects the end of the government shutdown; a lot of data will be obtained between now and the January FOMC meeting; the baseline expectation is for robust economic growth next year. Powell believes that rate hikes are not anyone's baseline scenario, and the current policy debate is between holding rates steady and cutting rates.

Powell also said that there is no risk-free policy path, and the risk balance has changed in recent months. The Fed has been adjusting toward a neutral rate and is now at the upper end of the neutral range, with no decision yet made for January. He emphasized that the Fed will make decisions meeting by meeting, and there is no predetermined path for monetary policy; the scale of Treasury purchases may remain high in the coming months. In the Q&A, Powell said he wants to leave the economy in a very good state when handing over to the next chair, hoping inflation is under control and back to 2%, and the labor market remains strong. Regarding his personal future, Powell said he has no new plans after his term as Fed Chair ends.

In the final months of his term as Fed Chair, Powell is trying to ensure a smooth landing. As Trump is about to announce his successor, the influence of the "shadow" Fed Chair is increasing. Powell's statements at this press conference were both expected and somewhat helpless.

IV. How to Interpret This Fed Decision

Regarding the Fed's final rate decision of the year, "Fed mouthpiece" Wall Street Journal reporter Nick Timiraos wrote that Fed officials cut rates for the third consecutive meeting, but there is unusual division within the Fed over whether inflation or the job market should be the bigger concern, so officials are not keen to continue cutting rates. In recent weeks, public comments by Fed officials have shown such severe internal division that the final decision may depend on how Chair Powell wants to proceed. Powell's term ends in May next year, meaning he will only preside over the next three rate-setting meetings. Stubborn price pressures alongside a cooling labor market present the Fed with an unpleasant trade-off not seen in decades. In the so-called "stagflation" period of the 1970s, when officials faced a similar dilemma, the Fed's stop-and-go approach allowed high inflation to become entrenched.

State Street Bank analyst Marvin Loh said that the Fed cut rates as expected, but this can only be interpreted as a hawkish move because officials did not change their forecasts for the next two years. He noted: "This will cause rates to drift very slowly toward the theoretical 3% neutral rate. Given the significant upward revision of GDP in the Summary of Economic Projections (SEP), the inclusion of the word 'extent' in the statement to describe additional policy adjustments suggests that some FOMC members are considering the actual necessity of reaching the current 3% long-term 'dot plot' target."

Charles Schwab analyst Richard Flynn said that by taking preemptive action, the Fed is sending a cautious signal in the face of rising downside risks, especially as global growth remains sluggish and policy uncertainty persists. For investors, this is a measured adjustment rather than a dramatic shift. While this rate cut may provide short-term support for risk assets and could trigger a seasonal "Santa Claus rally," volatility may remain high as the market assesses its impact on future policy and the broader economic outlook.

Goldman Sachs analyst Kay Haigh said that the Fed has reached the end of "preemptive rate cuts." She believes: "The next step depends on labor market data weakening further to justify additional near-term easing. The 'hard dissent' among voting members and the 'soft dissent' in the dot plot highlight the Fed's hawkish camp, and the reintroduction of wording about the 'extent and timing' of future policy decisions in the statement is likely to appease them. While this leaves open the possibility of future rate cuts, labor market weakness must reach a high threshold."

Informa Global Markets commented on Powell's latest remarks: So-called "hawkish rate cuts" are just that. Powell pointed out that there is tension between the Fed's dual mandate, but also admitted that there has been little change since the last meeting. His comments were generally similar to before. The most memorable line from the press conference was: "The current economy does not look like an overheated economy that would trigger labor-driven inflation."

Chris Grisanti, Chief Market Strategist at MAI Capital Management in New York, commented on the Fed rate decision: "The initial reaction was no surprise, rates were cut as expected. But looking ahead, there is a lot of uncertainty. As we move from today's rate cut toward 2026, the tailwind from rate cuts will become less reliable. This could be a problem. To go further— with the Fed's revised wording emphasizing uncertainty about the 'extent and timing' of future rate cuts, the Fed is actually signaling to the market: don't take rate cuts for granted. In my view, this means we will only see more rate cuts if the economy slows significantly. As an equity investor, I hope there are no rate cuts in 2026, because that would mean the economy is weakening. I'd rather have a robust economy than more rate cuts."

Analyst Anna Wong said: "My assessment is that the overall tone of the policy statement and updated forecasts is dovish—though there are some potentially hawkish signals. On the dovish side, the Committee sharply raised the growth trajectory, lowered the inflation outlook, and kept the dot plot unchanged. The FOMC also announced the start of reserve management purchases. On the other hand, a signal in the policy statement suggests the Committee favors a long pause in rate cuts." She continued: "Although the dot plot shows only one rate cut in 2026—while the market expects two—our view is that the Fed will ultimately cut rates by 100 basis points next year. This is because we expect weak job growth and currently see no clear sign of inflation reigniting in the first half of 2026."

Michael Rosen, Chief Investment Officer at Angeles Investments, said: "This rate cut was expected, so there were no surprises. The 25 basis point cut passed by a 9-3 vote, also as expected, with Schmid and Goolsbee supporting no cut, and Miran wanting a 50 basis point cut. Again, no surprises. The statement highlighted labor market weakness, which was the main reason for the 25 basis point cut. This detail was picked up by the market, suggesting the Fed may continue to ease policy, although the current expectation is only for one 25 basis point cut next year, which has not changed."

In addition, the Fed's 25 basis point rate cut is still not enough for Trump. On Wednesday afternoon, Trump said at a White House event that the 25 basis point cut was "a rather small number, could have been doubled—at least doubled." He also reiterated his long-standing criticism of Fed Chair Powell.

V. Where Will the Market Go Next?

After this Fed decision, where will major asset markets, including cryptocurrencies, go in the future? Let's look at the main analyses and interpretations.

1. CryptoQuant analyst Axel posted on social media that after bitcoin pulled back to $80,000, it has resumed its bullish structure. This move comes as the market has almost fully priced in the Fed's third consecutive rate cut, which will improve financial conditions and, with Powell not delivering a hawkish surprise, opens the window for further asset gains. After pulling back from the October peak to the $80,000 range, the price has shown a steady upward trend over the past 14 days.

2. Fidelity Digital Assets, a subsidiary of Fidelity, stated that with macro expectations shifting, bitcoin has regained upward momentum and is currently fluctuating in the $90,000 range. Trading data shows that around $85,500 (about 32% below the all-time high), about 430,000 bitcoins were bought, making this price an important support level. Market volatility has stabilized, and Fidelity will closely monitor the market's reaction to today's Fed meeting.

3. Matrixport released a chart analysis showing that bitcoin's implied volatility continues to decline, reducing the likelihood of a significant breakout at year-end. Today's FOMC meeting is the last major catalyst, but once the meeting is over, volatility is likely to continue declining until the holidays. Without new bitcoin ETF inflows to drive directional momentum, the market may return to range-bound trading. This outcome is usually associated with further volatility decay. In fact, this adjustment process is already underway, with implied volatility continuing to fall and the market gradually lowering the probability of an upside surprise at the end of December.

4. XWIN Research Japan's research shows that institutional investors are actively adjusting their positions. On-chain data shows that BTC balances on major exchanges are declining, while USDT and USDC reserves are rising, indicating that institutions are reducing risk exposure and accumulating stablecoins. The research points out that this pattern is similar to the period from August to October 2025: funding rates surged before the FOMC meeting and plummeted after the announcement, while bitcoin prices peaked and then fell. Currently, CME futures open interest is stagnant, and large spot holdings are stable, further confirming that professional funds are preparing for volatility. Analysts advise investors not to blindly chase the pre-meeting rally but to manage risk in advance, as market volatility around FOMC meetings usually expands sharply.

5. Binance founder Changpeng Zhao said at the Bitcoin Middle East Conference that bitcoin's "four-year cycle" may no longer apply and mentioned that as institutional participation increases, the market may enter a "supercycle." The so-called supercycle refers to the impact of institutional and regulated capital flows on the market, which is stronger than the traditional halving-driven price cycle. Zhao also said that discussions about national-level bitcoin reserves may spread. He suggested that if the U.S. starts discussing strategic reserves, other countries may follow suit.

6. ARK Invest founder Cathie Wood said that bitcoin's four-year cycle will be broken and we may have already seen the bottom of this cycle.

7. Liquid Capital founder Yilihua posted that for long-term spot investment, a few hundred dollars makes no difference. The reason ETH is currently significantly undervalued is due to macro expectations of rate cuts and liquidity easing, as well as increasingly crypto-friendly policies. From an industry perspective, stablecoins are growing long-term, and finance is moving on-chain. ETH's fundamentals are completely different now, and these factors are also why he is heavily invested in WLFI/USD1. After going all-in, the rest is up to time, and he will not trade in and out in the short term. Finally, he reiterated that spot volatility is large enough, so it's best not to play with contracts: first, most people lack the necessary skills and mentality; second, contracts are a game where nine out of ten lose, which drains energy that could be better spent developing off-exchange business.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The Federal Reserve cuts rates again but divisions deepen, next year's path may become more conservative

Although this rate cut was as expected, there was an unusual split within the Federal Reserve, and it hinted at a possible prolonged pause in the future. At the same time, the Fed is stabilizing year-end liquidity by purchasing short-term bonds.

Betting on LUNA: $1.8 billion is being wagered on Do Kwon's prison sentence

The surge in LUNA’s price and huge trading volume are not a result of fundamental recovery, but rather the market betting with real money on how long Do Kwon will be sentenced on the eve of his sentencing.

What is the overseas crypto community talking about today?

What have foreigners been most concerned about in the past 24 hours?

Behind the 15 million financing, does Surf aim to become an AI analyst in the crypto field?

Cyber co-founder starts a new venture.